Download de presentatie

De presentatie wordt gedownload. Even geduld aub

1

Global Finance Transformation at Vedior

2

Peter Rinkes Finance Director Europe Vedior

3

GLOBAL FINANCE TRANSFORMATION AT VEDIOR

12 December 2007 Peter Rinkes

4

AGENDA 1. INTRODUCTION VEDIOR 2. BUSINESS PERFORMANCE IMPROVEMENT 3. FINANCE FUNCTION TRANSFORMATION

5

VEDIOR In search of Excellence

6

In search of excellence in:

Business Performance Operating margin target 2008: 4.6% Finance Function Being a business partner

7

INTRODUCTION VEDIOR Vedior NV, headquartered in Amsterdam, is an international staffing services company providing flexible labour. Vedior operates in 50 countries worldwide: almost the whole of Europe, North and South America, Australia and New Zealand, South Africa, Middle East and Asia

8

VEDIOR: BUSINESS MODEL

Decentralized structure/nature 50 countries More than 200 entities/operating companies Small corporate Headquarter (40 employees) Relatively autonomous management structure Local responsibility Minority shareholders Multi branding

Relatively autonomous management structure. Local responsibility. Minority shareholders. Multi branding.")

9

MULTI BRANDING

10

A leading party in professional/executive recruitment

VEDIOR: SECTOR SPLIT A leading party in professional/executive recruitment Other Sectors 8% Healthcare 6% IT 9% Education 1% Traditional 64% Engineering 7% Accounting 5% Revenues : EUR 7.7 billion Net profit : EUR 186 million Number of offices : Number of countries: 50

11

VEDIOR: BUSINESS PERFORMANCE IMPROVEMENT

CURRENT STRATEGY Offer a full range of recruitment services to both local and international employers Enlarge share of specialist recruitment services Organic growth Acquisitive growth Profitability > market share

12

VEDIOR: BUSINESS PERFORMANCE IMPROVEMENT (2)

Operating margin targeting 2008: 4.6% Operational performance Q3-07 YTD: 4.2%

13

VEDIOR: BUSINESS PERFORMANCE IMPROVEMENT (3)

Dynamic industry: War for talent! Ongoing liberalisation of labour laws New lines of business ZZP vs. life time employment Fast growing global industry

14

Fast growing global industry

Number of Agency workers (daily FTE x 1,000) Forecast based on an annual average growth of 6.8% and impact of lifting restrictions (sectoral bans + reasons of use) Forecast based on an annual average growth of 6.8% (same trends as between 1998 and 2006; impact of regulation changes excluded) Source: SEO Economic Research – Amsterdam

Forecast based on an annual average growth of 6.8% and impact of lifting restrictions (sectoral bans + reasons of use) Forecast based on an annual average growth of 6.8% (same trends as between 1998 and 2006; impact of regulation changes excluded) Source: SEO Economic Research – Amsterdam.")

15

VEDIOR: BUSINESS PERFORMANCE IMPROVEMENT (4)

STRATEGIC REVIEW (announced 25 October 2007) Wide range review of business portfolio, organisational alignment and corporate roles Mobilization of Top 100 people from across the business (13 and 14 December 2007)

Wide range review of business portfolio, organisational alignment and corporate roles. Mobilization of Top 100 people from across the business (13 and 14 December 2007)")

16

Vedior and Randstad: Creating an industry leader

HR service market is relatively immature, growing and consolidating Together Randstad and Vedior will become the 2nd largest HR services company in the world Leadership positions in key markets in Europe and the Americas A global leader in professional segments A leader in inhouse services A truly diversified geographic mix Enhanced platform for growth in attractive markets such as Eastern Europe, India and Japan Diverse client base Transaction beneficial for Randstad shareholders as it offers enhanced growth prospects, EPS accretion immediately after completion, attractive returns and a more balanced business profile Transaction provides Vedior shareholders with a very attractive offer and at the same time the potential to participate in the future value creation arising from the combination

17

BEST PRACTICE: AUSTRALIA

FINANCE FUNCTION TRANSFORMATION (1) BEST PRACTICE: AUSTRALIA

BEST PRACTICE: AUSTRALIA.")

18

FINANCE FUNCTION TRANSFORMATION (2)

Self assesment Internal benchmarking Identifying and sharing best practices

19

Source: Estudios de Mercado

SESA Company Benchmarking EBIT Evolution (%) Source: Estudios de Mercado

Source: Estudios de Mercado.")

20

FINANCE FUNCTION TRANSFORMATION (3)

FEATURES HIGHEST RATED FINANCE FUNCTIONS Business Partnering High level (integrated) IT systems Shared services for other group/sister companies

IT systems. Shared services for other group/sister companies.")

21

FINANCE FUNCTION TRANSFORMATION (4)

BUSINESS PERFORMANCE OF HIGHEST RATED FINANCE FUNCTIONS EBIT Top 3 Companies Gross Profit Top 3 Companies EBIT Worst Companies Gross Profit Worst 3 Companies

22

FINANCE FUNCTION TRANSFORMATION (5)

ISSUES CEO commitment ICT Staff capability Process of change management ‘Control’ requirements (company structure/corporate governance)

")

23

FINANCE FUNCTION TRANSFORMATION (6)

Geneva Second Global Finance Conference Evaluation self assesment Self assesment FFMG Strategic Review Vedior Paris First Global Finance Conference Kick off Sydney Start up fixing project Start up local Excellence projects Sept 2005 June 2006 Sept 2006 Jan 2007 July 2007 Dec 2007 2008

24

VEDIOR In search of Excellence

25

In search of excellence in:

Business Performance Operating margin target 2008: 4.6% Finance Function Being a business partner

26

Thank you for your attention

27

Rob Leicher Group Controller & VP Finance OPG Group

28

OPG Finance Finance Transformation Conference December 12, Rob Leicher Group Controller

29

Active in 8 countries Direct and Institutional Pharmacy

Norway Pharmacy, Direct and Institutional Denmark Holland Poland Germany Belgium Switzerland Hungary

30

Key Figures 2006 Net Sales 2,281 Operating result 130 Net result 100

X € million Net Sales 2,281 Operating result Net result Capital employed Number of employees at year end 6,686 Impact of strategy on your own role should be clear Building of a chain – much more than visual aspects; very muh about people International expansion – reducing the dependency on Holland OPG International (PLN/BEL) sofar not very succesful economically 30 30

sofar not very succesful economically")

31

Summary of OPG Strategy

Build retail pharmacy chains Mediq – NL, PLN, BEL Expand home care activities Dia Real , Kirudan, JP Medical, Other Improve efficiency Organisational Integration (Pre-)Wholesale PLN Pharmacies NL Impact of strategy on your own role should be clear Building of a chain – much more than visual aspects; very muh about people International expansion – reducing the dependency on Holland OPG International (PLN/BEL) sofar not very succesful economically 31 31

Wholesale PLN. Pharmacies NL. Impact of strategy on your own role should be clear. Building of a chain – much more than visual aspects; very muh about people. International expansion – reducing the dependency on Holland. OPG International (PLN/BEL) sofar not very succesful economically")

32

CONTROLLED GROWTH More countries Increasing complexity

More standardisation required Best practice sharing Back-office integration; focus on efficiency Integration of new companies incl. synergy creation More standardised and integrated IT Development of new competencies required Business models differ per bu; best practice sharing only recently started eg visits pharmacists PLN/NL, but still very unstructured Logistics started a little; process analysis 32 32

33

ROLES OF FINANCE FUNCTION AT OPG

Presentatie Controllers'workshop - March 28, 2007 4 april 2017 ROLES OF FINANCE FUNCTION AT OPG Current role ORIENTATION Aspiration CONTROL BUSINESS Short term “Controller” “Performance manager” HORIZON “Builder” Finance has an integrated and comprehensive view of the business; natural role as sparring partner of BU manager “Planner” Long term 33 FER/07.072 33

34

ROLES OF FINANCE FUNCTION AT OPG

Presentatie Controllers' workshop - Jube 14, 2007 4 april 2017 ROLES OF FINANCE FUNCTION AT OPG ORIENTATION CONTROL BUSINESS ‘Controller’ Enhanced transparency and compliance Audit Risk Matrix Embedded Control Self Assessment ‘Performance manager’ Activity Based Costing and cost control Outsourcing Working capital reduction SHORT TERM HORIZON ‘Planner’ Strategic milestone tracking Improved forecasting Tax planning ‘Builder’ M&A Business integration Financial market communication Financial management development LONG TERM 34 FER/07.112 34

35

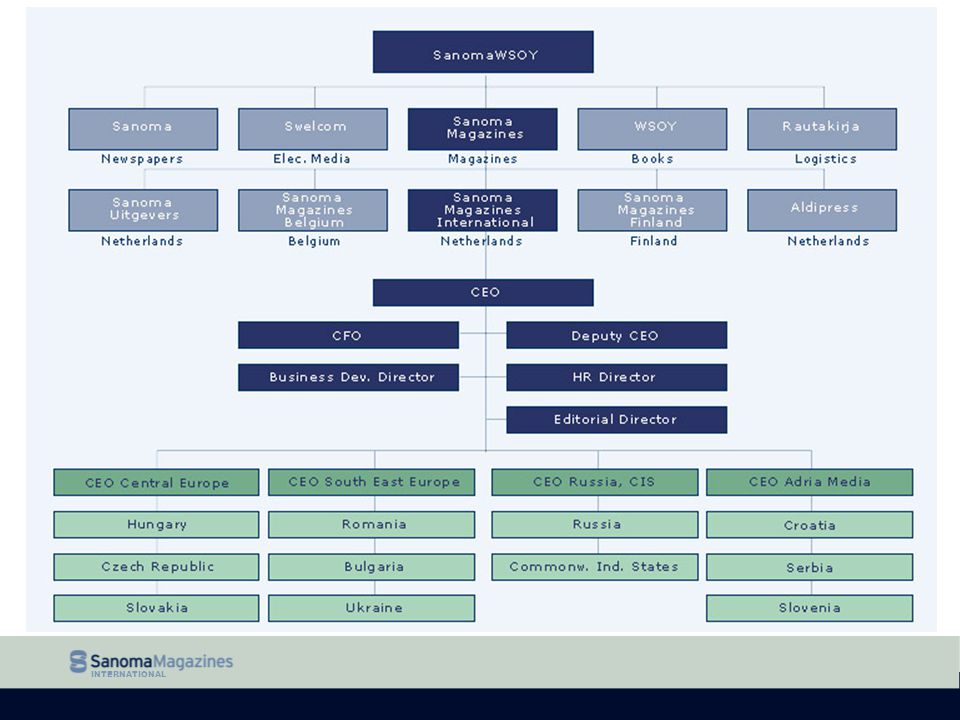

Peter Mannaert CFO Sanoma Magazines International

36

Parallelsessie global finance transformatie

Peter Mannaert, CFO Sanoma Magazines International

37

Sanoma Magazines International

■ Uitgeverij van tijdschriften ■ Zusterbedrijf van Sanoma Uitgevers (libelle, margriet, donald duck, ilse, nu.nl, startpagina etc.) ■ Actief in 10 landen in Centraal, Oost en Zuid-Oost Europa, local player ■ > 20% groei per jaar ■ Fully owned dochters, maar ook veel JV’s Kengetallen Sanoma Magazines 2006: ■ € 1,218.9 miljard netto omzet ■ € miljoen EBIT ■ medewerkers ■ SMI ; fte’s wv 8 op HQ

■ Actief in 10 landen in Centraal, Oost en Zuid-Oost Europa, local player ■ > 20% groei per jaar ■ Fully owned dochters, maar ook veel JV’s. Kengetallen Sanoma Magazines 2006: ■ € 1,218.9 miljard netto omzet ■ € miljoen EBIT ■ medewerkers ■ SMI ; fte’s wv 8 op HQ.")

40

Business Transformation: Uitdagingen voor CFO SMI

Business partner ; meedenken over strategie en organisatie Groei van de onderneming eist een meer volwassen aanpak Acquisitieplannen ; focus vs verbreding Kostenbeheersing blijft belangrijk Loonontwikkeling CEE Efficiency slagen Benchmarking, proces assesments Kennis uitwisselen/ best practice sharing Verbetering (Corporate) Performance Management Een versie van de werkelijkheid Minder excel Betere managementinfo Effectiever budgetteren

Performance Management. Een versie van de werkelijkheid. Minder excel. Betere managementinfo. Effectiever budgetteren.")

41

Werkveld CFO SMI Situatieschets Dilemma’s Financial Accounting

Concernrapportages strak georganiseerd (Hyperion) Management Accounting Eigen invulling BU’s Geen centrale CIO Board van Divisiedirecteuren Locale P&L verantwoordelijkheid Doelstellingen Groei Professionalisering AO/IC Managementrapportages IFRS Opleidingsniveau CFO’s Dilemma’s Groei vs KT winst Centraal/ Decentraal ; SSC voor Admin , IT ? Wie neemt risico’s/ investeringen Geen gezamenlijk IT platform BI platform of lokaal Excel Uniformiteit in Management Acc. Multimedia ; nwe diensten of focus Procesoptimalisatie vs local for local Geen gezamenlijk IT platform SM Divisies ; zelf ontwikkelen ?

Management Accounting. Eigen invulling BU’s. Geen centrale CIO. Board van Divisiedirecteuren. Locale P&L verantwoordelijkheid. Doelstellingen. Groei. Professionalisering. AO/IC. Managementrapportages. IFRS. Opleidingsniveau CFO’s. Dilemma’s. Groei vs KT winst. Centraal/ Decentraal ; SSC voor Admin , IT Wie neemt risico’s/ investeringen. Geen gezamenlijk IT platform. BI platform of lokaal Excel. Uniformiteit in Management Acc. Multimedia ; nwe diensten of focus. Procesoptimalisatie vs local for local. Geen gezamenlijk IT platform SM Divisies ; zelf ontwikkelen")

42

Een excellente finance functie is een katalysator van excellente business performance

43

Contracten met nieuwe klanten zijn altijd resultanten van een afgewogen en evenwichtig besluitvormingsproces

44

Een decentraal opgezette functie heeft zijn langste tijd gehad

45

Finance is voorloper van transformaties/change

46

Customer value en profitabilty is moeilijk integraal te benaderen

47

De CFO moet zich meer focussen op finance en minder op andere domeinen

48

De CFO heeft een sturende rol om andere staffuncties naar een hoger niveau te tillen

49

Alle staffuncties zouden in een shared service omgeving beter bijdragen aan de business

Verwante presentaties

, de Vlaamse Gemeenschap, de Stad Antwerpen, OCMW.>")