Download de presentatie

De presentatie wordt gedownload. Even geduld aub

1

De bankcrisis: Oorzaken, gevolgen en oplossingen Paul De Grauwe

2

Oorzaken Essentie van bankieren Banken “borrow short and lend long” Dit creëert grote broosheid Geen probleem in normale tijden wanneer mensen vertrouwen hebben Probleem ontstaat als vertrouwen zoek is Dit kan gebeuren als één of meer banken solvabiliteitsproblemen kennen (voorbeeld: slechte leningen )

")

3

Oorzaken Dan is een “bank run” mogelijk: liquiditeitscrisis Sleept ook andere “onschuldige” banken mee Er ontstaat een duivelse interactie tussen liquiditeits- en solvabiliteitscrisis: solvabele banken moeten activa verkopen om terugtrekken van deposito’s op te vangen Deze verkopen doen prijzen activa dalen Waarde van de activa van de banken daalt solvabiliteitsprobleem En nieuwe liquiditeitscrisis

4

Oorzaken De bankcrisis van de jaren Dertig en de Grote Depressie hadden geleid to hervormingen die de banksector minder broos moesten maken Deze zijn Centrale bank als “lender of last resort” Deposito verzekering Splitsing commerciële- en zakenbanken (Glass-Steagall Act 1933)

")

5

Meeste economen dachten dat dit zou volstaan om veiligheid in te bouwen in bankstelsel En om grote bankcrisis onmogelijk te maken Dat was dus niet zo Waarom? Laten we eerst begrip “Moral Hazard” introduceren

6

Moral Hazard De verzekering die impliciet geboden wordt door centrale banken en overheden heeft een sterke prikkel gegeven aan bankiers om meer risico te nemen. Om dit tegen te gaan hebben overheden banken onderworpen aan toezicht en controle gedurende de naoorlogse periode Maar dan gebeurde iets merkwaardigs.

7

Het nieuwe paradigma van de efficiënte markten Het paradigma werd erg populair ook buiten academische ivoren toren Belangrijkste ingrediënten: Prijzen weerspiegelen fundamentele waarden; dus zeepbellen kunen niet ontstaan Financiële markten kunnen zichzelf reguleren; er is geen overheidsregulering nodig

8

Bankiers waren entousiast Paradigma van efficiënte markten was erg invloedrijk Bankiers gebruikten het om te pleiten voor deregulering Ze haalden hun slag thuis Banken in VS en Europa werden geleidelijk gedereguleerd Hoogtepunt van deregulering: Afschaffing van Glass-Steagall act in 1999 (Clinton-Rubin-Summers)

")

9

Banken konden nu alle activiteiten, traditioneel gereserveerd voor zakenbanken, opnemen Underwriting en beleggen in aandelen en derivaten en nieuwe financiële producten met hoog risico De les van de Grote Depressie was vergeten

10

Andere factor: financiële innovaties Deregulering van financiële markten viel samen met proces van financiële innovatie En werd er ook door versterkt Financiële innovatie bracht nieuwe financiële producten die toelieten traditionele leningen te verpakken in verschillende risico-klassen en te verkopen in de markt “Securisering” (“securitisation”)

")

11

Andere factor: financiële innovaties Men dacht dat deze complexe producten het risico zouden spreiden over meer actoren (efficiënte marktidee) met minder systeemrisico tot gevolg En dus minder noodzaak voor toezicht en regulering De markt zou zichzelf wel reguleren

met minder systeemrisico tot gevolg En dus minder noodzaak voor toezicht en regulering De markt zou zichzelf wel reguleren")

12

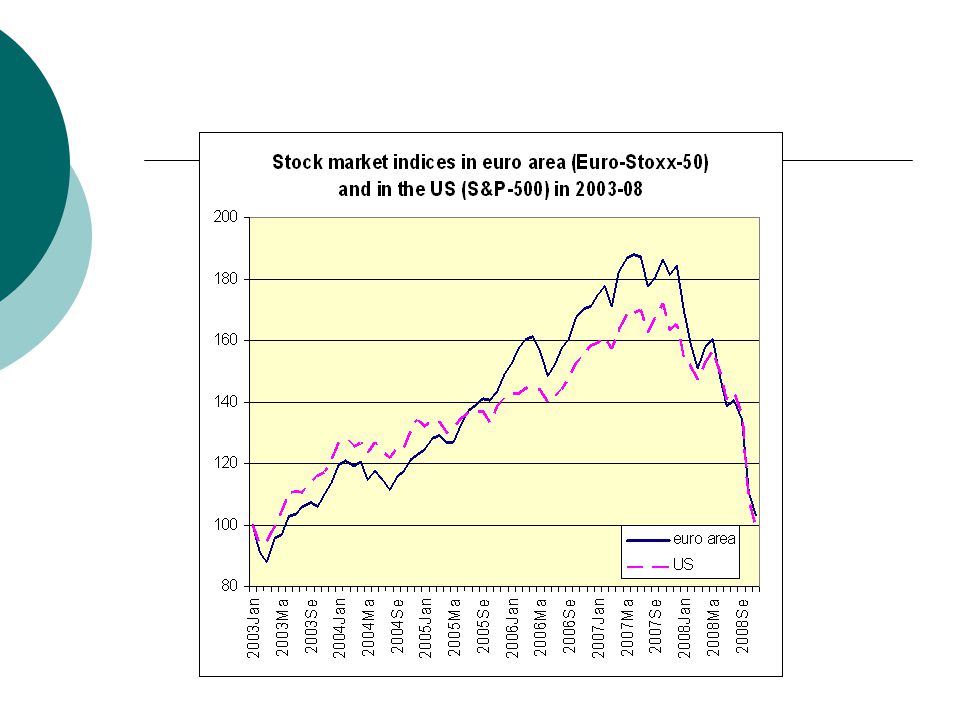

Zijn financiële markten wel efficiënt? De te verwachten wonderen van deregulering waren gebaseerd op het bestaan van efficiënte markten Zijn die wel efficiënt? Antwoord: zeepbellen en ineenstortingen (“Bubbles and crashes”) maken inherent deel uit van kapitalisme

maken inherent deel uit van kapitalisme.")

14

Nasdaq :similar story

15

Vastgoedmarkt in de VS

16

wisselmarkten

17

“Bubbles and crashes” zullen niet verdwijnen “Bubbles and crashes” zijn het resultaat van grote onzekerheid Beleggers zijn genoodzaakt gebruik te maken van “heuristics”. Voorbeeld: koop als prijs stijgt Of koop als “goeroe” het zegt dit leidt tot kuddegeest Kindleberger, Manias, Panics and Crashes: bubbles and crashes hebben bestaan sinds het begin van kapitalisme en zullen niet verdwijnen

18

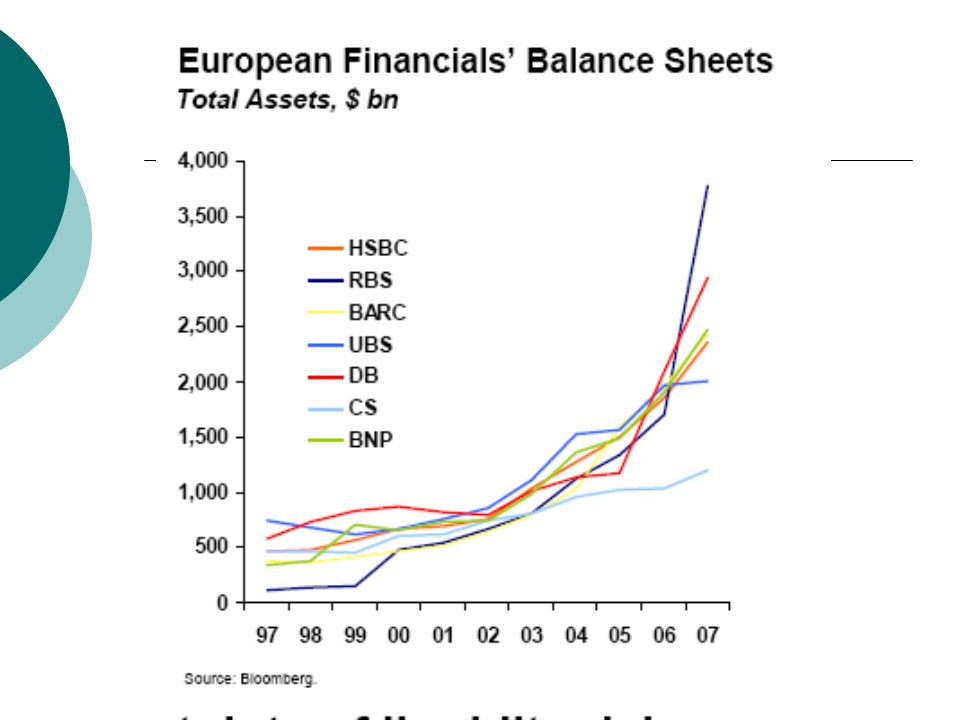

Banken surfen op bewegingen van financiële markten Ten gevolge van deregulering konden banken het hele gamma van financiële producten aanhouden Ze werden dus meegesleurd door de grote speculatieve bewegingen Hun balansen werden hypergevoelig voor de zeepbellen (hi-tech zeepbel, immobiliën zeepbel, grondstoffenzeepbel) Bankbalansen kenden inflatie

Bankbalansen kenden inflatie")

21

Het omgekeerde is ook waar De balansen van de banken werden ook heel gevoelig voor de crash. De trigger was de crash in de huizenmarkt in de VS Dit was slechts een trigger De crisis zou in elk geval ontstaan zijn

22

Additional developments: regulatory arbitrage Basle I was an attempt to impose similar capital ratios in all developed countries’ banks It was based on a classification of assets according to risk and to force banks to set capital aside against these assets based on the risk

23

Regulatory arbitrage: case 1 Basle I put a low risk weight on loans by banks to other financial institutions This gave incentives to bank to transfer risky assets (e.g. structured products) with high risk weight off their balance sheets in special conduits to which they extended short- term credit Banks were doing favour to each other As a result increasingly banks obtained their funding through the interbank (wholesale) market which is not insured by government High leverage

with high risk weight off their balance sheets in special conduits to which they extended short- term credit Banks were doing favour to each other As a result increasingly banks obtained their funding through the interbank (wholesale) market which is not insured by government High leverage.")

25

Regulatory arbitrage: case 2 Basle I made it possible for banks to treat assets that are insured as government securities, i.e. zero risk weight This led to explosion of CDS (credit default swaps) Created the illusion in banking system that the assets on their balance sheets had low risk This turned out to be wrong. Why?

Created the illusion in banking system that the assets on their balance sheets had low risk This turned out to be wrong. Why .")

26

Private insurance does not insure against tail risk very well Financial models used to price CDS (but also other financial products, e.g. derivatives) are based on normal distribution of returns There is one general feature in all financial markets: returns are not normally distributed Returns have fat tails (bubbles and crashes) Implication: models based on normal distribution dramatically underestimate probability of large shocks

are based on normal distribution of returns There is one general feature in all financial markets: returns are not normally distributed Returns have fat tails (bubbles and crashes) Implication: models based on normal distribution dramatically underestimate probability of large shocks.")

27

Example: stock market (DJ) Changes that are higher than 5 standard deviations occur once every 7000 years if returns are normally distributed During the last 80 years there were 76 such changes What should we conclude?

Changes that are higher than 5 standard deviations occur once every 7000 years if returns are normally distributed During the last 80 years there were 76 such changes What should we conclude")

28

Was last October exceptional? Yes, if you have studied finance theory and believe returns are normally distributed No if you have not studied finance theory

29

As a result, there is systematic underpricing of risk (tail risk) creating a perception of low-risk environment In addition, there were no incentives to price this tail risk because there was implicit expectation that if something very bad would happen, e.g. a liquidity crisis (a typical tail risk) central banks would provide the liquidities This created the perception in banks that liquidity risk was not something to worry about.

central banks would provide the liquidities This created the perception in banks that liquidity risk was not something to worry about..")

30

Samengevat Deregulering, Afwezigheid van voldoende toezicht Het toepassen van een foute theorie Financële innovaties (securitisation) Moral hazard Bracht banken ertoe ongehoorde risico’s aan te gaan De balansen waren vervlochten met de zeepbelbewegingen in de markten En ontploften als de markten crashten.

Moral hazard Bracht banken ertoe ongehoorde risico’s aan te gaan De balansen waren vervlochten met de zeepbelbewegingen in de markten En ontploften als de markten crashten.")

31

The reaction of the authorities: central banks Learning by doing: Massive liquidity provision by central banks, Provided the necessary liquidity and prevented liquidity crisis from bringing down the whole system But they also stretched balance sheets of central banks

32

The reaction of the authorities: governments Government guarantees on interbank deposits were essential in preventing freezing of interbank market from leading to large scale liquidity crisis But are they credible?

33

But are they credible?

34

The reaction of the authorities: governments Recapitalization of banks :They have been massive Together with the previous interventions, these have been successful up to now in averting a bank collapse but it is unclear whether they will be sufficient to avert future crises and to bring the banking system back on track so that it can perform its function of credit creation

35

Fundamental problem banks face today balance sheets are massively inflated because of their participation in consecutive bubbles. banks face a period during which their balance sheets will shrink substantially (“deleveraging”). This process is will not be a smooth one

. This process is will not be a smooth one.")

36

mainly because during the shrinking the devilish interaction of solvency and liquidity crises will occur. This is likely to create a further downward spiral. As a result, there is as yet no floor on the value of the banks’ assets. Governments will be called upon again to recapitalize And nationalize banks It’s not yet over

37

Worse to come Deleveraging will give strong incentives to banks not to extend new loans, thereby dragging down the real economy. How far and how long this will go, nobody knows. It is not inconceivable that this leads to a long and protracted downward movement in economic activity.

38

What can be done: short run A return of Keynesian economics. Governments will be forced to sustain demand in the face of dwindling tax revenue Thus massive budget deficits are likely and desirable Attempts at balancing government budgets would not work, as it would likely lead to Keynes’ savings paradox.

39

What can be done: short run In the process of recapitalizing banks, governments will substitute private debt for government debt. This also is inevitable and desirable. As agents distrust private debt they turn to government debt deemed safer. Governments will have to accommodate for this desire. (See Hyman Minsky (1986) on this)

on this).")

40

What can be done: short run Governments and central banks will also have to support asset prices, in particular stock prices by buying assets Recapitalizing banks is clearly insufficient to stop the liquidity- solvency spiral.

41

Long-term reform Back to narrow banking We have to go back to narrow banking Strict separation of commercial and investment banking The classes of assets in which banks can invest must be limited No securitization anymore Higher liquidity ratios And less leverage Alternative of Basle II does not work

42

Investment banks can do all the sophisticated asset creation and management but must fund these through the capital market with liabilities of same maturity. No short-term funding possible No funding through commercial banks

43

Banking will become much less profitable but less risky bankers will scream

44

International coordination at setting new rules will be necessary Otherwise race to the bottom leading to new deregulation International coordination of rule setting is most challenging

Verwante presentaties

![Deltion College Engels C1 Gesprekken voeren [Edu/002]/ subvaardigheid lezen thema: Order, order…. can-do : kan een bijeenkomst voorzitten © Anne Beeker.](/8/2048322/big_thumb.jpg "Deltion College Engels C1 Gesprekken voeren [Edu/002]/ subvaardigheid lezen thema: Order, order…. can-do : kan een bijeenkomst voorzitten © Anne Beeker.>")