Download de presentatie

De presentatie wordt gedownload. Even geduld aub

2

De geschiedenis De logica Intuitie creativiteit

3

Idealen (vrede, welvaart) verwezenlijken Instrument: tijdgeest beter lezen dan rest structurele mogelijkheden onderkennen

verwezenlijken Instrument: tijdgeest beter lezen dan rest structurele mogelijkheden onderkennen")

4

1. Eurocrisis 2. Gevolgen machtsverschuivingen in Midden Oosten voor onze energievoorziening

5

Positief: Duitsland is in euro te sterk, wordt door Energiewende zwakker Negatief: Zuidelijke landen eurozone zijn veel kwetsbaarder voor olieprijs stijging dan Noorden. Door aanslag kan prijs stijgen

6

Eurozone komt goed: grand bargain is steun in ruil voor hervormingen Politieke unie is onvermijdelijk maar burgers willen niet, dus stiekem Niet politiek orgaan ECB vangt klappen op

7

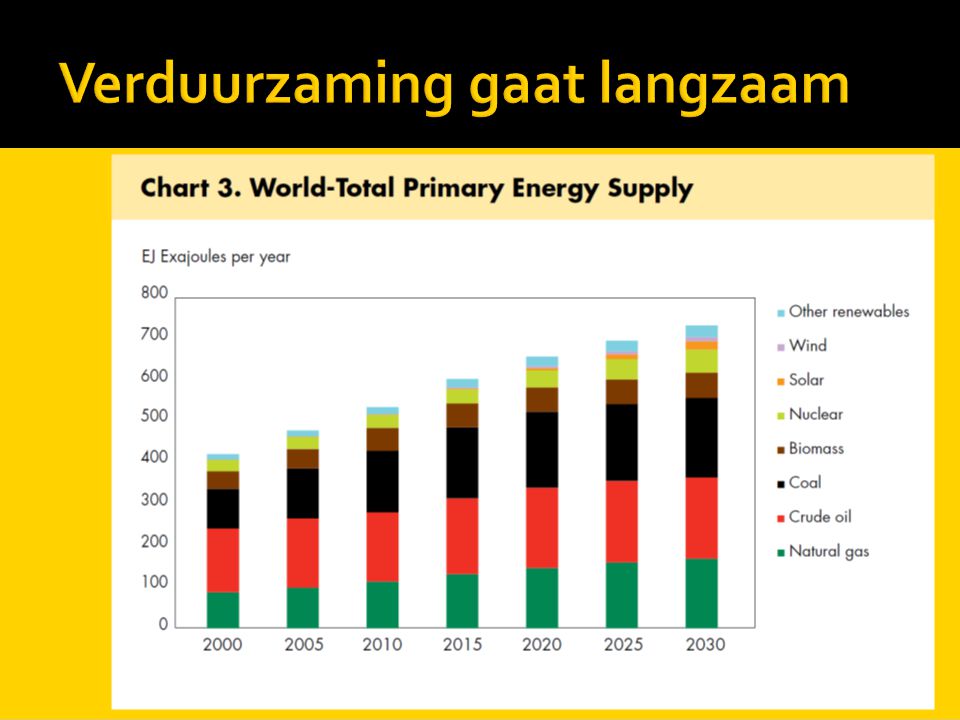

Energie moet duurzamer maar niet te snel Nu 25 % Duitse stroom zon, wind, biomassa Duitse stroom duur, bruinkool en gas springen bij NL 2020 14% duurzaam in 2023 16%. Duitsland 2020 45% energie duurzaam EU 2010 12,5 %, 2011 13,4 %, 2020 20 %

9

Dat kan alleen als: 1. Zuiden convergeert met Noorden 2. er politieke unie komt 3. instituties in Zuiden sterker worden 4. banken gesaneerd worden en geherkapitaliseerd

10

Er is wel beetje convergentie Concurriekracht divergeert nog 25 %

11

1. Noorden wil grip op beleid Zuiden en geen onbeperkte steun 2. Zuiden wil beleidsvrijheid plus onbeperkte steun 3. grote vraag is of Merkel omgaat

12

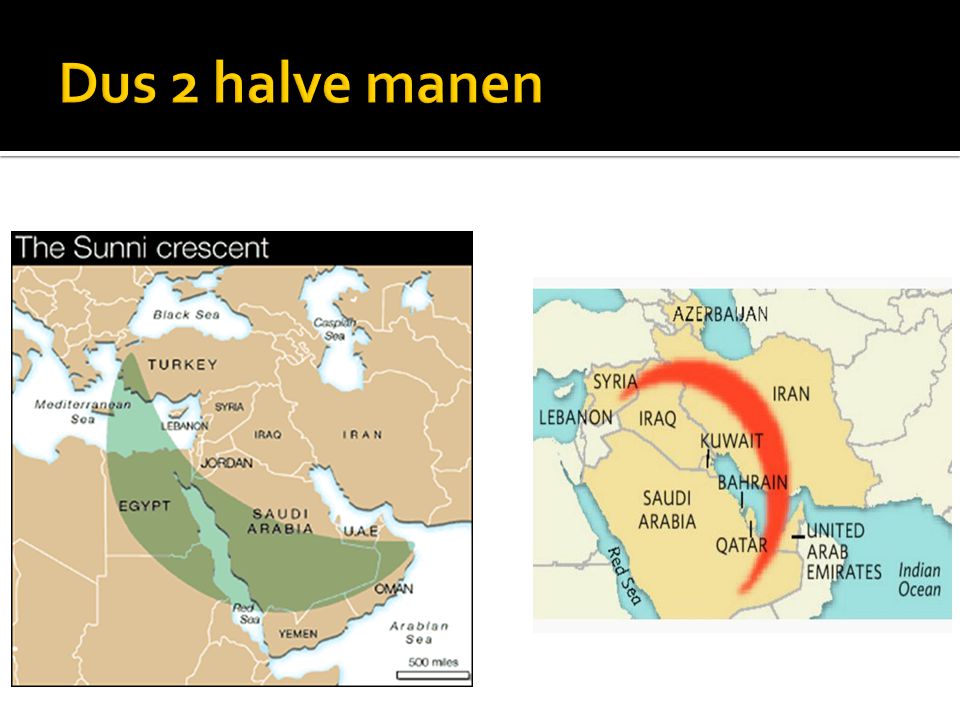

1. kapitaal/arbeid is Zuiden gepolariseerd 2. boete/schuld versus eer/schaamte 3. meritocratie versus clientelisme Frankrijk: grandeur/soevereiniteit/etatisme Spanje: post-Franco orde: decentralisatie! Maar euro vraagt om centralisatie Italië: etatisme, clientelisme, patronage, corruptie Griekenland: nog erger Italië

13

Sterke banken lobby Merkel durft zelfs Landerbanken niet aan te pakken Nog steeds geen waarheidsgetrouwe stresstest Europese bankenunie vereist eerst sanering

14

1. te weinig convergentie 2. geen consensus politieke unie 3. instituties Zuiden blijven zwak 4. banken sanering onduidelijk

15

Argumenten tegen ontbinding: 1. ontbinding is gewoon te kostbaar 2. crisis maakt burgers offerbereid 3. neuro is devaluatie: slechts tijdelijke oplossing 4. Euro succes nodig om EU machtsverval <

16

Argumenten voor ontbinding 1. euro 17 is te heterogeen, historisch, cultureel, politiek, institutioneel 2. zelfs politieke unie kan zwakke instituties niet versterken 3. steun vermindert prikkel om hervormen 4. Zuiden kan devaluatie Zuiden politiek niet missen

17

NL kan niets zonder DTSL We moeten in ieder geval met DTSL nadenken over alternatieven, bijv. parallel currencies Deadline 5 jaar Maar wordt een puinhoop!

18

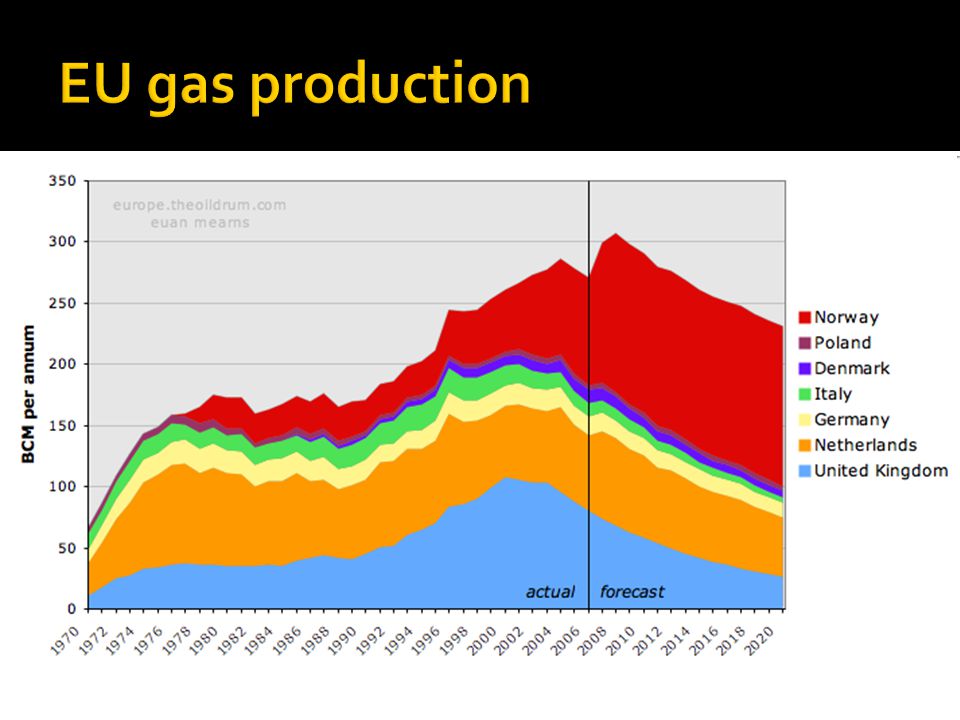

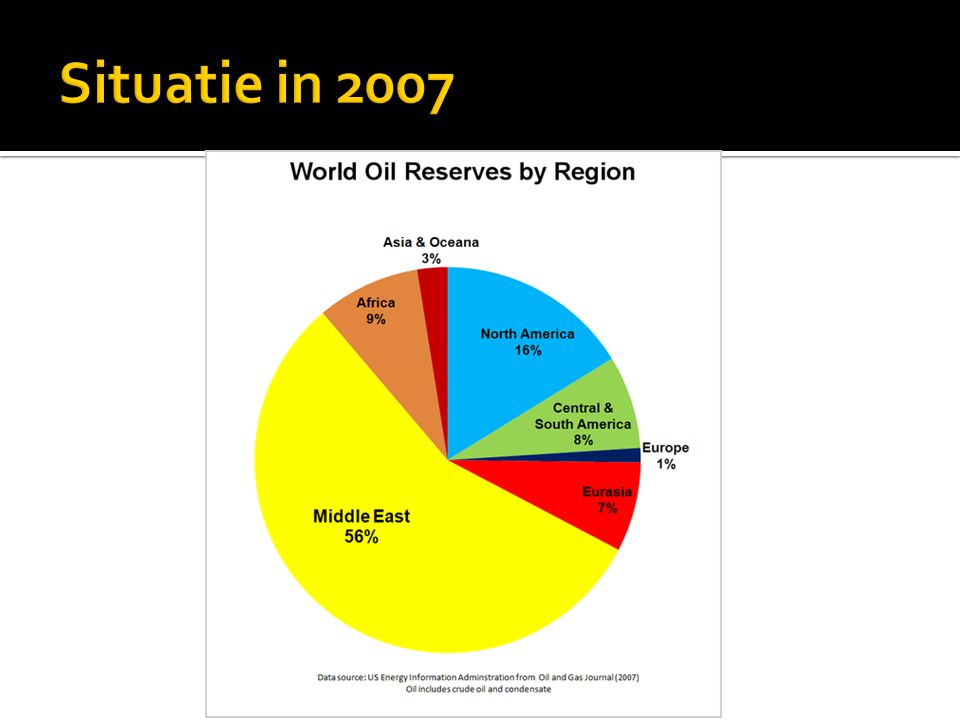

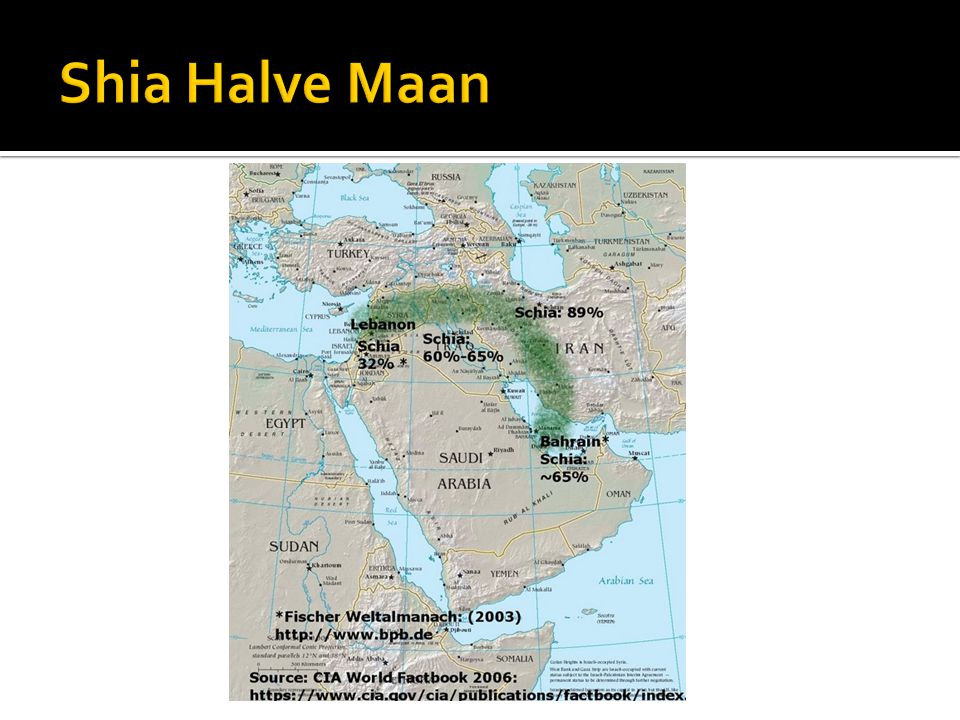

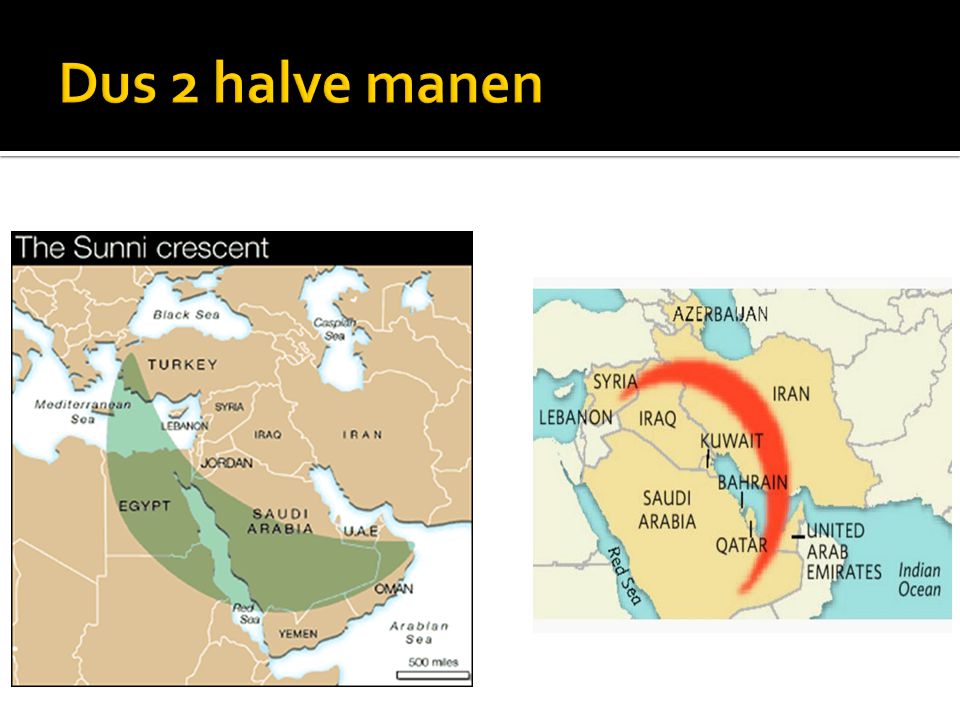

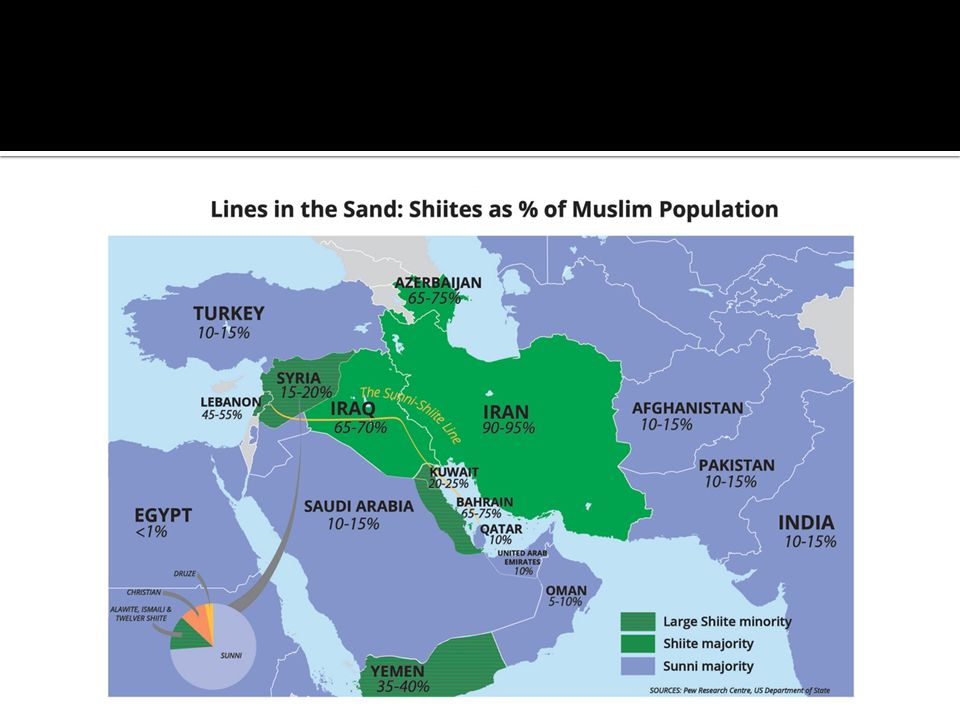

Zuiden is nog meer afhankelijk van het Midden Oosten dan Noorden van Europa

20

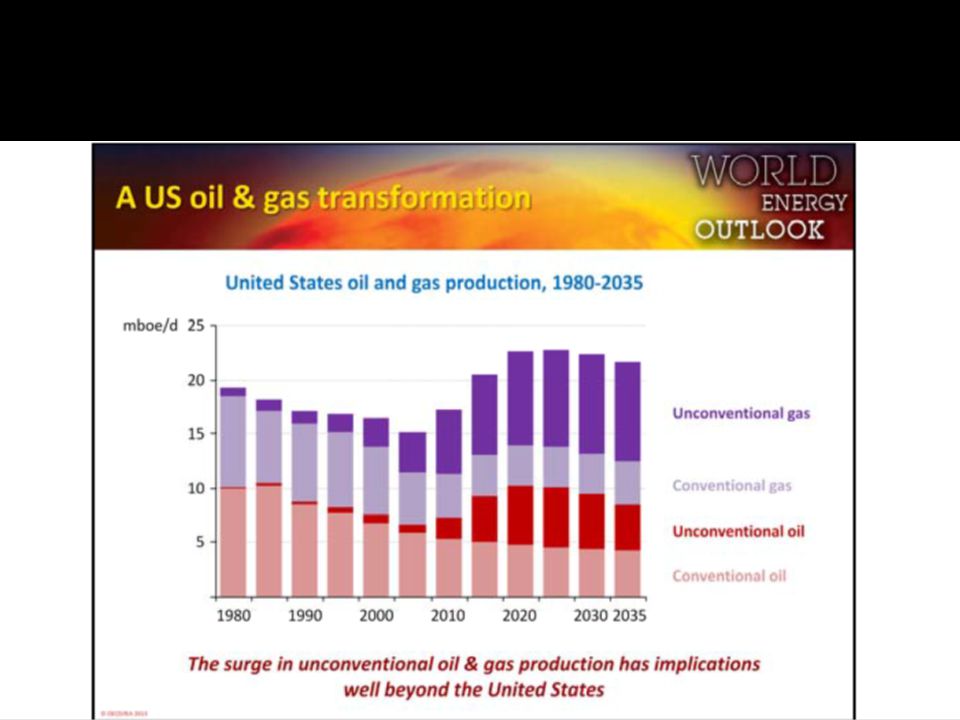

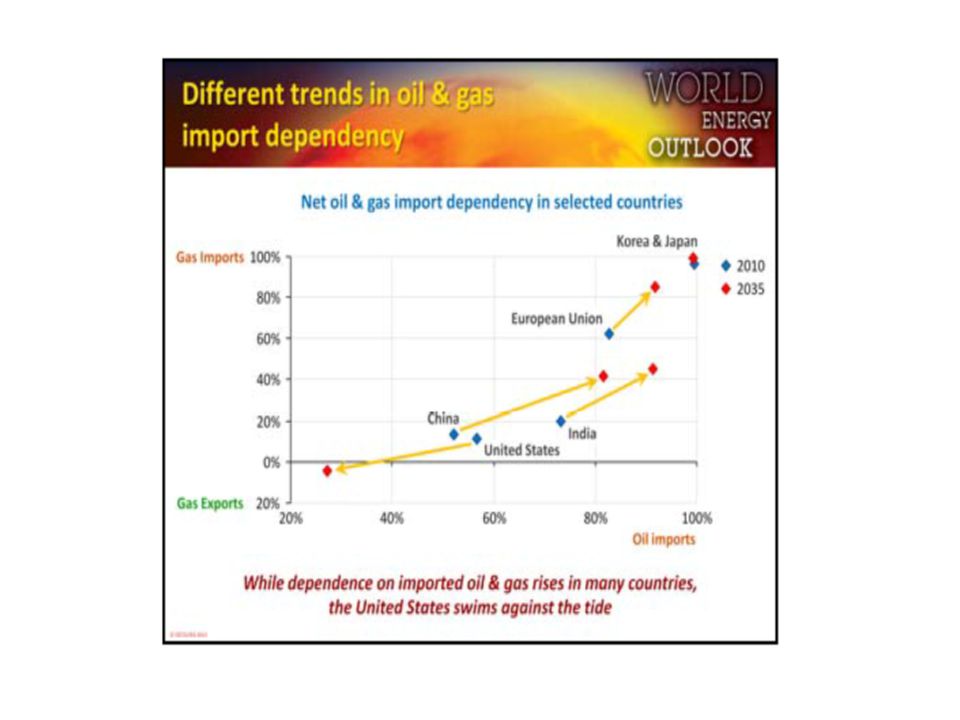

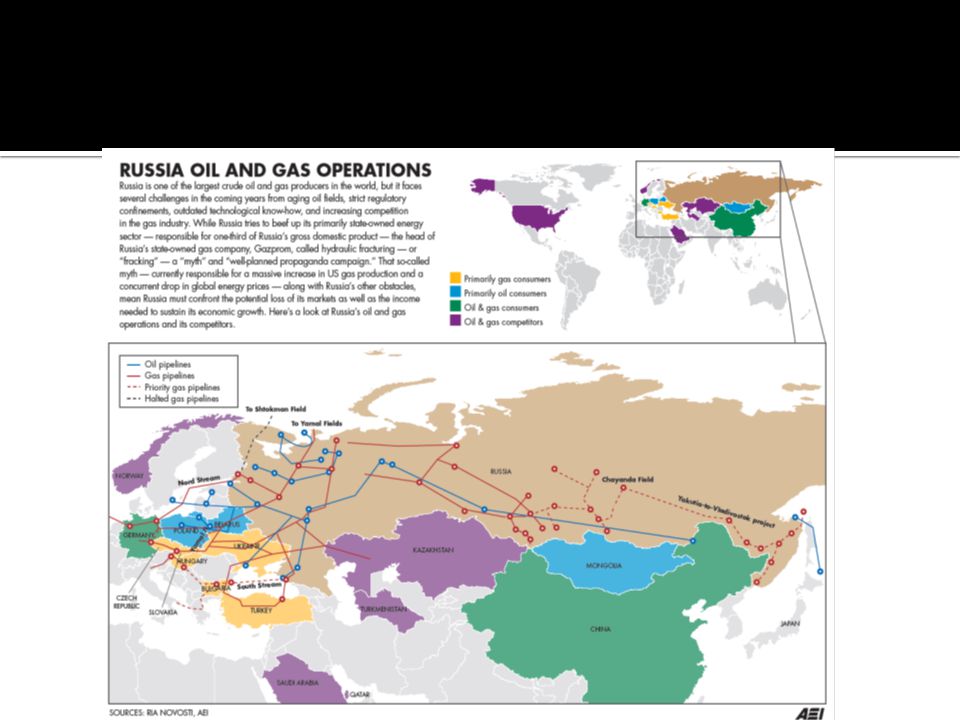

2020 -50 %, 2035 VS onafhankelijk van MO olie door: 1. VS schaliegas 2. Canada teerzand, schaliegas 3. Brazilie 4. duurzame energie China en EU blijven afhankelijker MO olie/gas

24

Arabische lente in Jemen en Saoedi Arabië kan prijs crude oil > Schaliegas is problematisch: aardbevingen, grondwatervervuiling

25

VK deed het van 1700 tot 1940 Na 1945 East of Suez debate Na WO II USA Gaat VS dat nu gratis voor EU/ China doen?

43

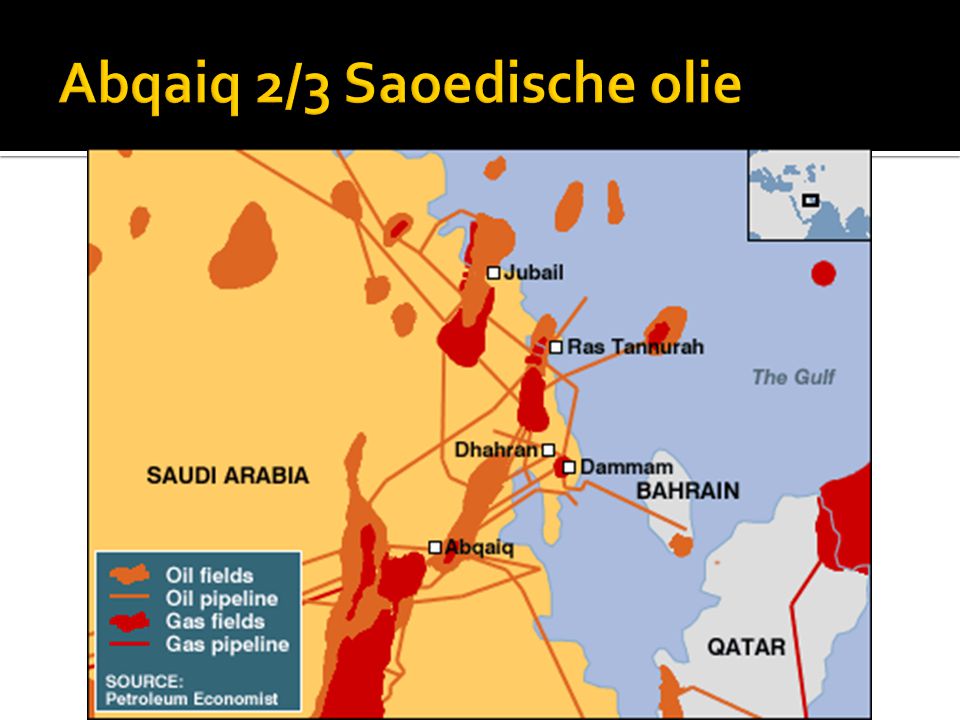

De wereldvraag ca. 86 miljoen vaten olie per dag. In het ergste geval zou een aanslag op Abqaiq - tijdelijk - 6 miljoen vaten per dag kunnen kosten dat is 7% van de totale wereldwijde dagelijkse olie consumptie! Gevolg olieprijs > Pijnlijkste voor Zuid-Europa (Eurocrisis >)

.")

46

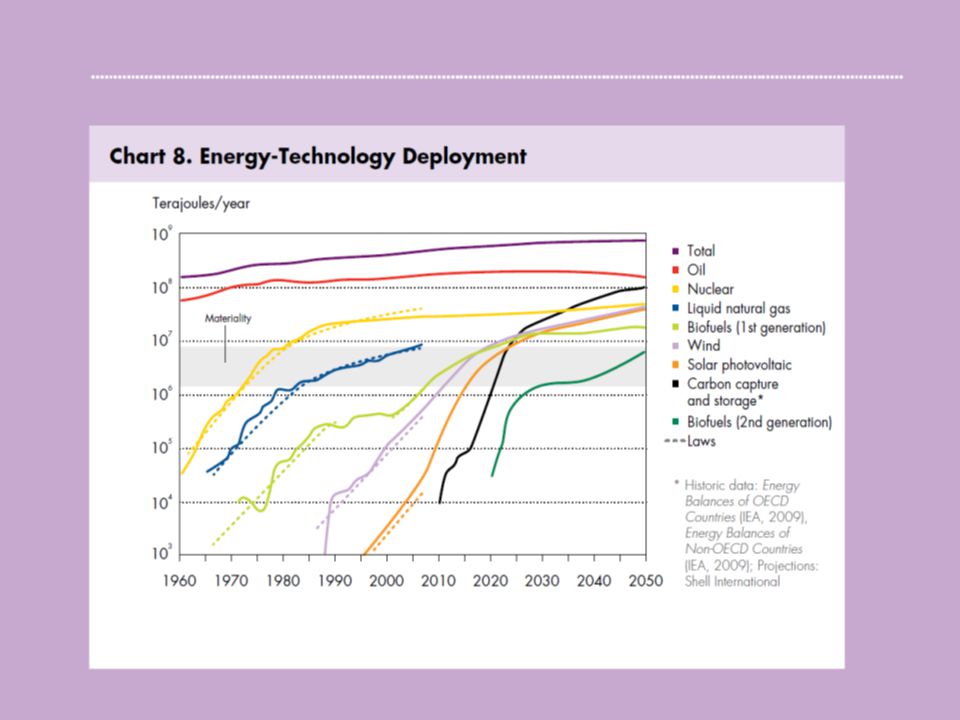

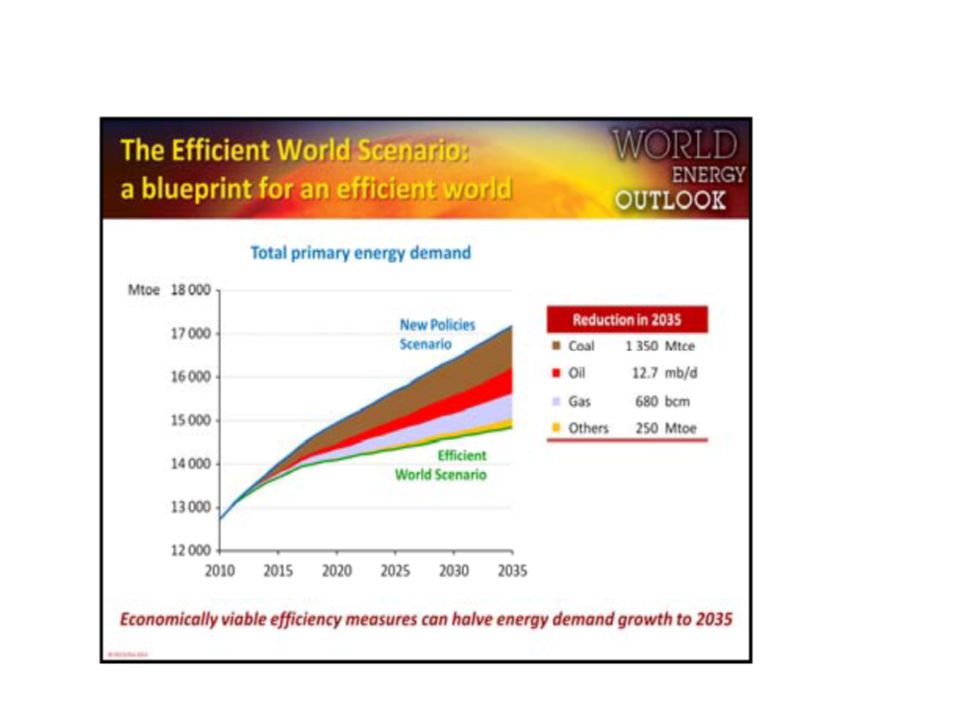

groei energievraag zit in non-OECD: Azië en China groei energievraag vnl kolen en aardgas. Duurzame energie groeit hard, maar is klein op wereldschaal. Wat Duitsland doet is druppel op gloeiende Chinese plaat. duurt 30 jaar voordat nieuwe energie technologie doorbreekt. (1000-fold growth needed) 30 jaar pilot-plant scale up to 1-2% of the world’s total primary energy requires a sustained growth rate of 26% per annum

30 jaar pilot-plant scale up to 1-2% of the world’s total primary energy requires a sustained growth rate of 26% per annum.")

49

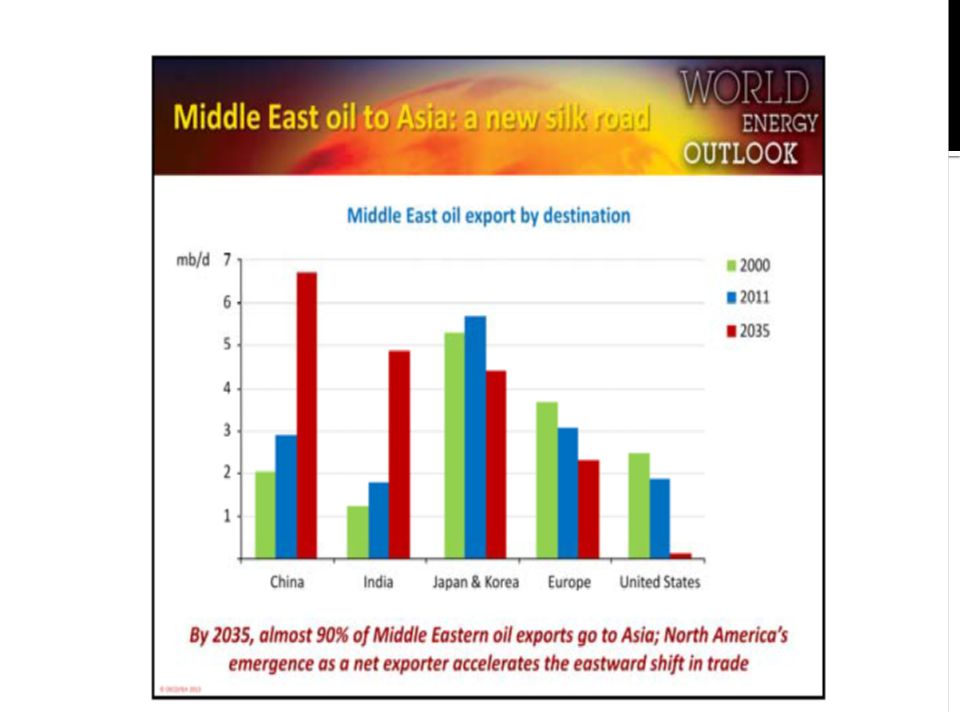

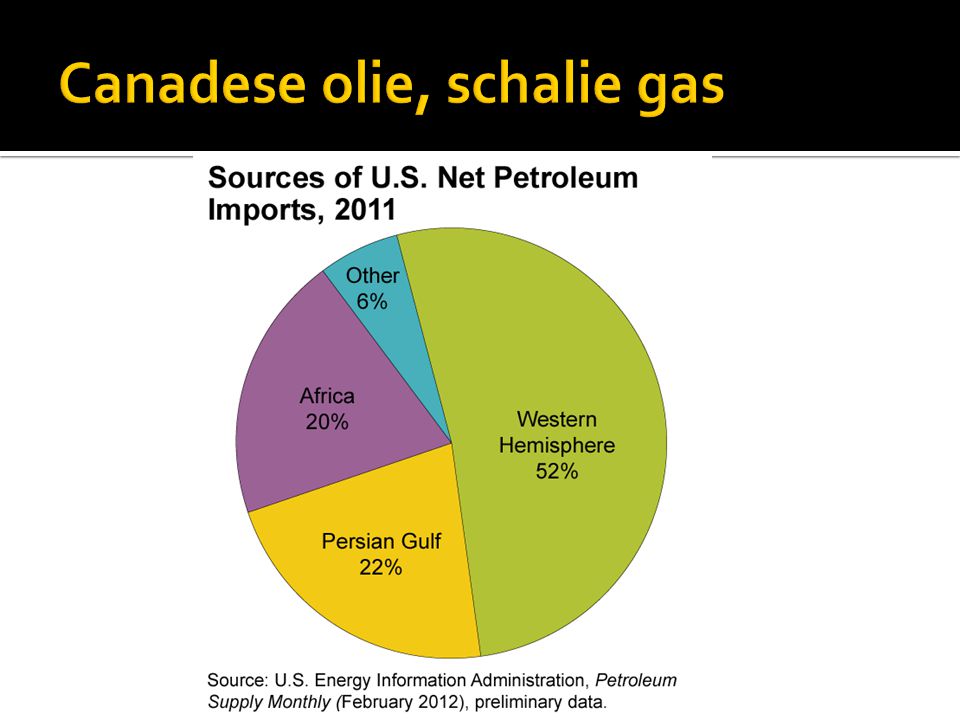

2006, Middle East 22 % of U.S. imports, 36 % of Europe's, imports 2012 US imports 17 %, European 29 % > US will import 2035 0% Middle East 2020 America produceert meer olie dan SA

52

Shaliegas en olie zal prijs < Minder inkomsten Golf staten Dus minder handouts aan bevolking Dus instabiliteit China/EU heeft geen militaire footprint in MO China slurpt alles op en houdt handouts in stand

53

Many analysts believe that a unified global pricing structure for fossil fuels will keep America engaged, but with U.S. spot prices for natural gas currently running at a fraction of what the fuel costs in Europe and East Asia, it appears global pricing isn’t so integrated after all.

56

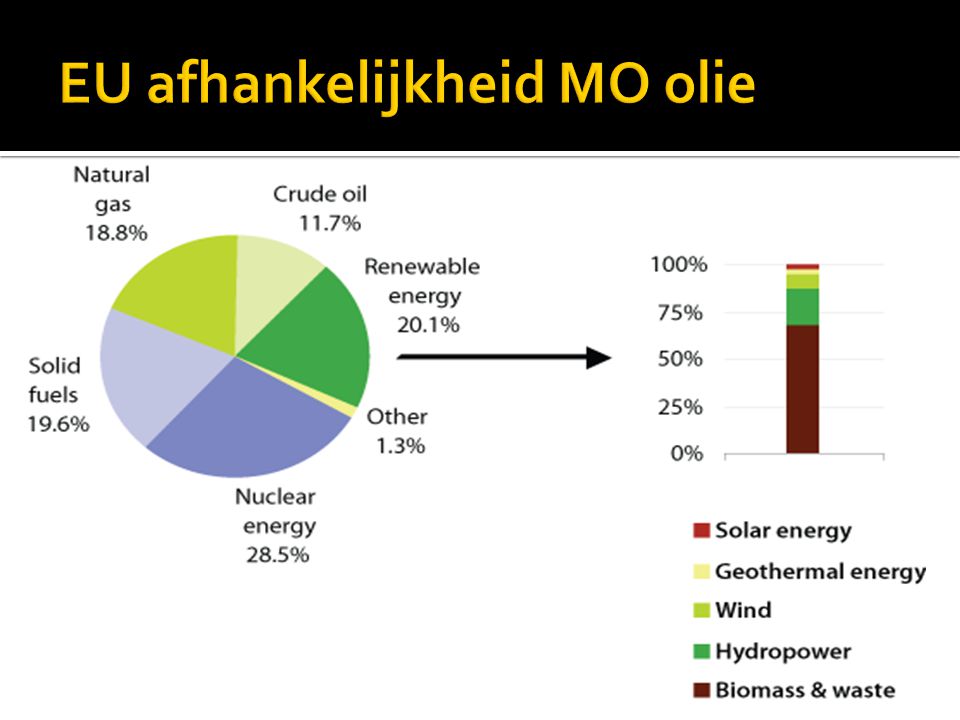

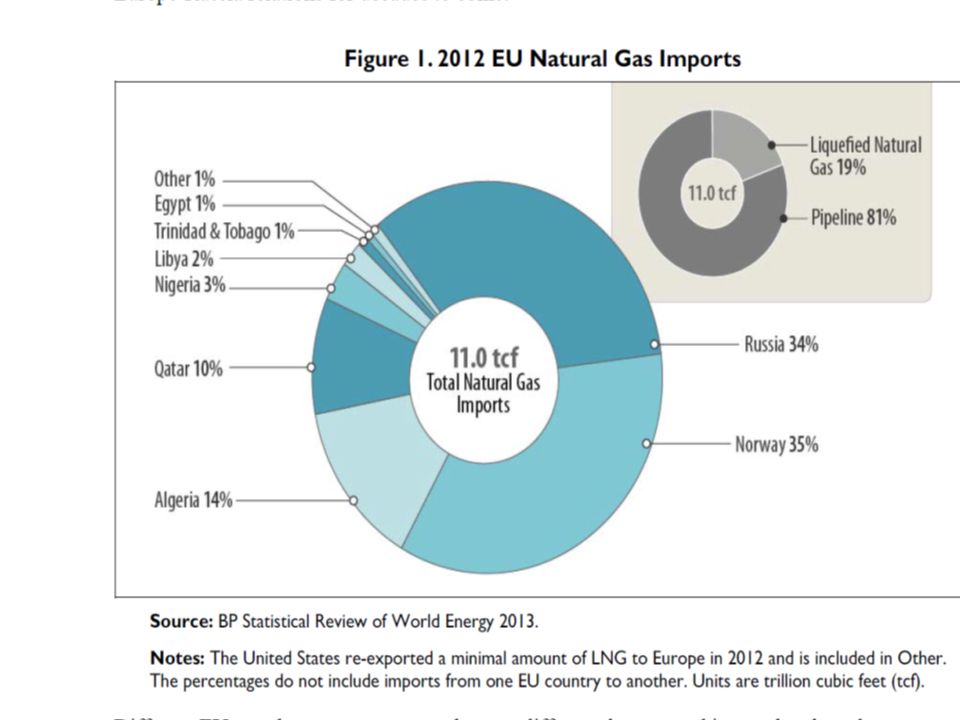

the EU’s increasing dependency on energy imports from non-member countries. Indeed, more than half (54.1 %) of the EU-27’s gross inland energy consumption in 2010 came from imported sources. Echter slechts 15,63 % van Midden Oosten

of the EU-27’s gross inland energy consumption in 2010 came from imported sources. Echter slechts 15,63 % van Midden Oosten.")

57

Since November, the United States has replaced Saudi Arabia as the world's biggest producer of crude oil. It had already overtaken Russia as the leading producer of natural gas. The United States imports over three-times more oil from Canada than it does from Saudi Arabia

58

USA 22 % of its oil imports ME, it will < Europe imports 15,63 % ME, it will > Europe imports 80 percent of its oil and 60 percent of its natural gas — a third of that comes from Russia. the world's largest shale gas resources are believed to lay deep below the soil of China.

60

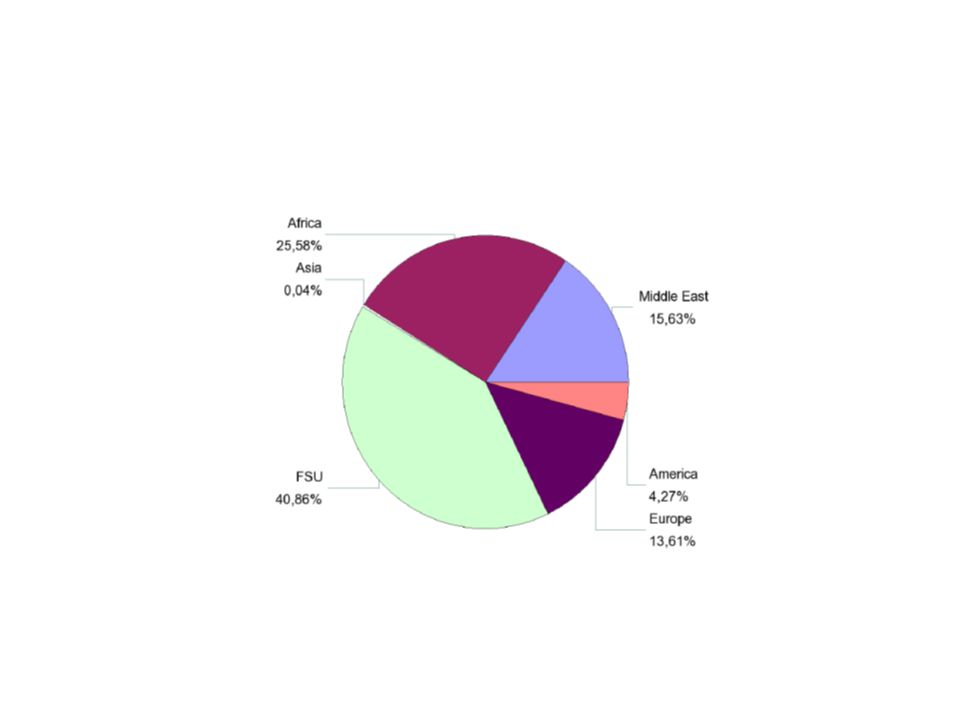

Middle East 15,63 % Africa 25,58 % FSU 40,86 % Europe 13,61 % America 4,27 %

70

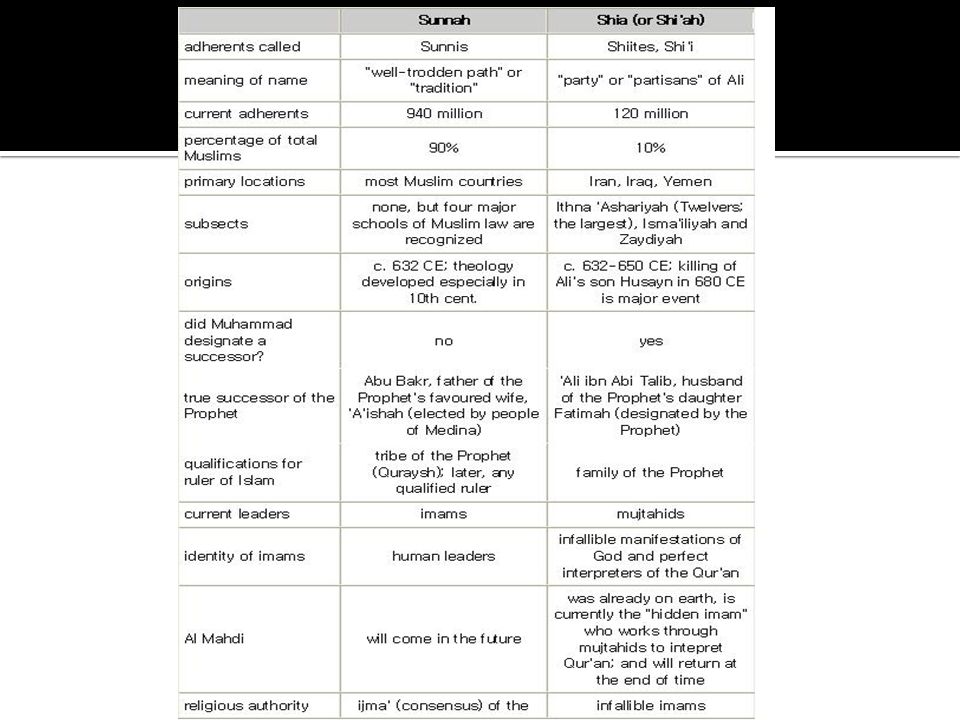

on Feb. 15 when Iran’s Oil Ministry threatened to cut off exports to six European countries in a bid to preempt the EU embargo on oil imports from Iran, First, note which European countries Tehran threatened with its oil-export ban: France, Greece, Italy, the Netherlands, Portugal, and Spain. 4 PIGS!

71

the PIIGS also run a massive deficit with the oil-producing countries of the world, and especially those of the Middle East. According to the CIA, oil imports by those countries were around 4.6 million barrels a day in 2008. For the EU as a whole the figure was 18.2 million, of which just under a third came from the Middle East and North Africa. (The U.S. imported 11.3 million barrels a day, with around a fifth from those regions.)

.")

72

True, Iran is not a huge exporter to Europe. According to the U.S. Department of Energy, total Iranian sales to the EU averaged 450,000 barrels a day last year. But more than 70 percent went to Italy and Spain, while a third of Greek oil imports came from Iran. The case of Portugal is especially interesting, since if Greece is kicked out of the euro zone (as seems increasingly likely), Portugal will be next in line. In December 2011, its trade deficit with six oil-exporting countries was more than double the size of its deficit with Germany.

, Portugal will be next in line. In December 2011, its trade deficit with six oil-exporting countries was more than double the size of its deficit with Germany..")

74

De Amerikanen rekenen er zelfs op tegen 2020 nog amper energie te moeten invoeren.

75

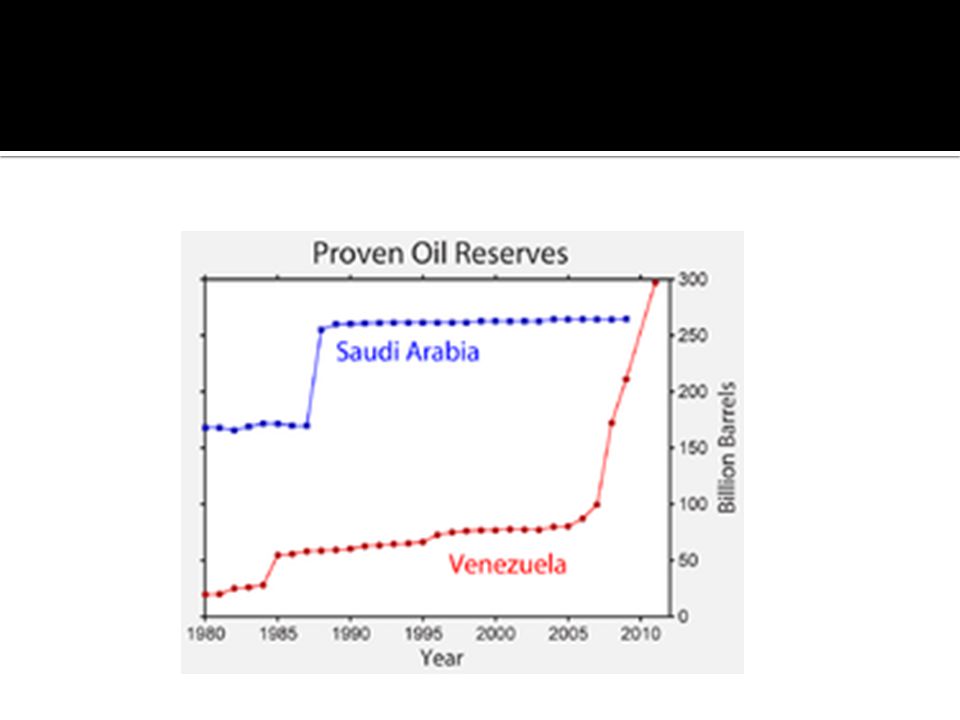

Middle East - 16 (Iraq - 2, Kuwait - 4, Lebanon - 5, Saudi Arabia - 1, Turkey - 4) Africa and North Africa – 18 (Algeria - 3, Angola - 6, Congo - 1, Mozambique - 3, South Africa - 2, Sudan - 3) Latin America – 29 (Argentina – 2, Colombia – 19, Ecuador – 2, Guatemala – 1, Peru – 2, Suriname - 1, Venezuela – 20) North America – 2 (US – 1, Canada - 1) Europe – 17 (Belgium – 3, Cyprus – 1, Germany – 7, Norway – 1, Spain – 4 UK – 1) Asia – 6 (Afghanistan - 2, Japan - 2, Philippines - 1, Thailand - 1)

Africa and North Africa – 18 (Algeria - 3, Angola - 6, Congo - 1, Mozambique - 3, South Africa - 2, Sudan - 3) Latin America – 29 (Argentina – 2, Colombia – 19, Ecuador – 2, Guatemala – 1, Peru – 2, Suriname - 1, Venezuela – 20) North America – 2 (US – 1, Canada - 1) Europe – 17 (Belgium – 3, Cyprus – 1, Germany – 7, Norway – 1, Spain – 4 UK – 1) Asia – 6 (Afghanistan - 2, Japan - 2, Philippines - 1, Thailand - 1)")

76

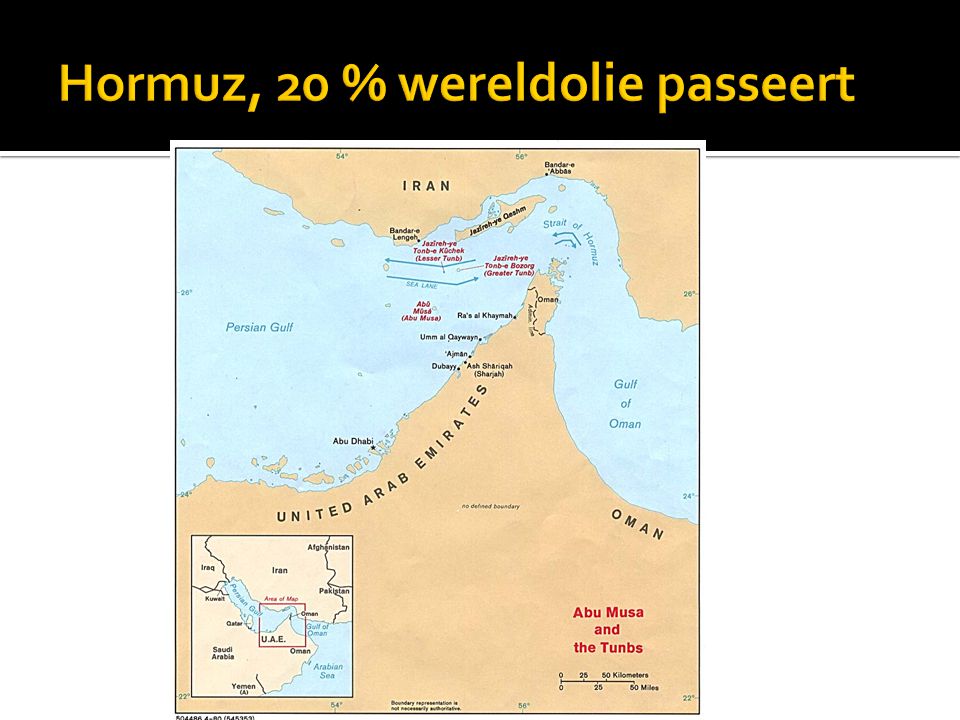

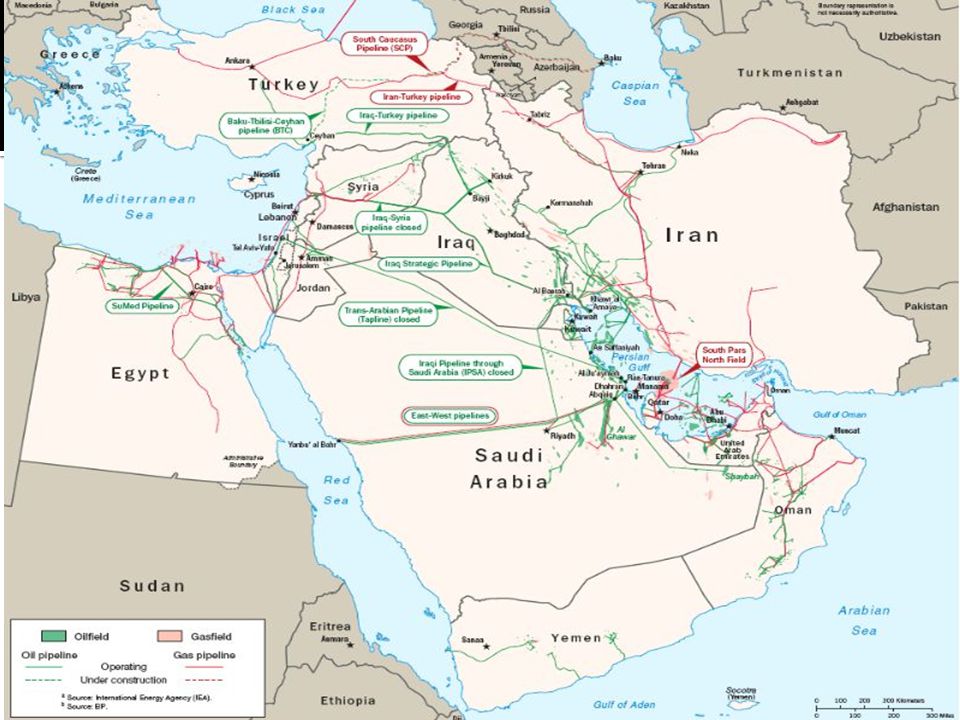

On the Persian Gulf, Saudi Arabia has just two primary oil export terminals: Ras Tanura - the world's largest offshore oil loading facility, through which a tenth of global oil supply flows daily - and Ras al-Ju'aymah. On the Red Sea, a terminal called Yanbu is connected to Abqaiq via the 750- mile East–West pipeline. A terrorist attack on each one of these hubs of the Saudi oil complex or a simultaneous attack on few of them is not a fictional scenario. A single terrorist cell hijacking an airplane in Kuwait or Dubai and crashing it into Abqaiq or Ras Tanura, could turn the complex into an inferno. This could take up to 50% of Saudi oil off the market for at least six months and with it most of the world’s spare capacity, sending oil prices through the ceiling.

85

VS steeds minder belang bij rol politie agent Europa/China geen militaire footprint Geopolitieke reden voor duurzame energie Maar dat duurt lang China koopt steeds meer olie/gas, regimes MO gaan door met handouts bevolking Arabische lente?

86

1. eurozone 17 is te heterogeen 2. energieafh. Zuiden maakt nog heterogener 3. Sunni-Shia divide kan energiestromen belemmeren, probleem Eurozone 4. herschikking is onvermijdelijk 5. herschikking is kostbaar 6. dus geopolitieke reden Energiewende 7. Energiewende duurt echter EU/China langer dan in VS

87

1. China met schaliegas zal bloeien 2. fantastische grondstoffenpolitiek, rare earth etc. 3. voorlopers duurzame energie 4. door crisis in Westen: alternatief democratie interessanter 5. vergrijzing < 2 kindpolitiek

88

Vergrijzing Crisis democratie Problemen versterkt door relatieve verarming

Verwante presentaties

>")

![Deltion College Engels C1 Gesprekken voeren [Edu/002]/ subvaardigheid lezen thema: Order, order…. can-do : kan een bijeenkomst voorzitten © Anne Beeker.](/8/2048322/big_thumb.jpg "Deltion College Engels C1 Gesprekken voeren [Edu/002]/ subvaardigheid lezen thema: Order, order…. can-do : kan een bijeenkomst voorzitten © Anne Beeker.>")

to watch throughout the month of August,>")

Quiz Night !>")