Download de presentatie

De presentatie wordt gedownload. Even geduld aub

1

Waardering van lineaire rente-instrumenten

The Financial Markets Academy / Thomson Reuters 8 oktober 2010

2

Programma Implied forward rates Zero coupon rates Waardering Duration

Toepassingen op renteswaps

3

Forward yields

4

Implied forward yield 3-mnds rente = 1,00 6-mnds rente = 1,10 ?

5

Implied forward yield money market (FRA contract rate)

accumulation factor = / = /360 x forward rate 1 183 365 accumulation factor = /360 * 0.011 accumulation factor = /360 * 0.012

6

Calculation method of money market forward forward rates

1 + (rl x dl/year basis) ( -1 ) x year basis / df rf = 1+ (rs x ds/year basis)

( -1 ) x year basis / df. rf = 1+ (rs x ds/year basis)")

7

Implied forward yield capital market – forward periods start after one year

accumulation factor = / = (1 + forward rate)2 1.0404 1 2 yr 4 yr accumulation factor = ( )2 accumulation factor = ( )4

yr. 4 yr. accumulation factor = ( )2. accumulation factor = ( )4.")

8

Calculation method of capital market forward forward rates

(1 + rl)l Year basis/f ( ) -1 rf = (1+ rs)s

l. Year basis/f. ( ) -1. rf = (1+ rs)s.")

9

Implied forward yield capital market – forward period starts within first year

accumulation factor = = (1 + forward rate)2 1 183 days 2 yr, 182 days accumulation factor = ( /360 x 0.011) accumulation factor = ( )2,5

days. 2 yr, 182 days. accumulation factor = ( /360 x 0.011) accumulation factor = ( )2,5.")

10

Calculation method of capital market forward forward rates

(1 + rl)l Year basis/f ( ) -1 rf = 1+ (rs x ds/year basis)

l. Year basis/f. ( ) -1. rf = 1+ (rs x ds/year basis)")

11

Implied forward yield money market – forward period starts after one year

accumulation factor = / = ( /360 x forward rate) 1 3,5 yr 4 yr accumulation factor = ( )3,5 accumulation factor = ( )4

,5 yr. 4 yr. accumulation factor = ( )3,5. accumulation factor = ( )4.")

12

Calculation method of money market forward forward rates

(1 + rl)l ( - 1) x year basis / df rf = (1+ rs)s

l. ( - 1) x year basis / df. rf = (1+ rs)s.")

13

Ontleden van de spot rate in implied forward rates

3 mnds rente over 3 mnd over 9 mnd over 6 mnd 3 mnds rente 6 mnds rente 9 mnds rente 12 mnds rente

14

21s v 24s FW 18s v 21s FW 15s v 18s FW 2.40 2.30 2.20 2-jaars spot rate 2% 2.00 1.90 1.75 1.65 1.55 12s v 15s FW 9s v 12s FW 6s v 9s FW 3s v 6s FW 3m EURIBOR

15

Waardering rentedragende producten

Zero couponrente en effectief rendement

16

Waarderen van renteproducten

Beursproducten: Beurskoers OTC: Contante waardemethode Bepaal de toekomstige cashflows Maak deze contant met de zero-couponrentes Tel de contante waarden op

17

Waardering marktconforme staatsobligatie 08/11 – 2,78%

Yieldcurve: 1 jaar 2,29% 2 jaar 2,59% 3 jaar 2,78% 1027,8 27,8 27,8 1 2 27,05 26,32 946,64 27,8/(1 + 0,0278) 27,8/(1 + 0,0278)2 1000,- 1027,8/(1 + 0,0278)3

27,8/(1 + 0,0278) ,- 1027,8/(1 + 0,0278)3.")

18

Strips Separate Trading of Registered Interest and Principal Securities

Yieldcurve: 1 jaar 2,29% 2 jaar 2,59% 3 jaar 2,78% 1000 ?

19

Strips Separate Trading of Registered Interest and Principal Securities

Yieldcurve: 1 jaar 2,29% 2 jaar 2,59% 3 jaar 2,78% 27,8 27,8 27,8 1 2 3 ? ? ?

20

Welke rente gebruiken bij afzonderlijke cashflows?

Yieldcurve: 1 jaar 2,29% 2 jaar 2,59% 3 jaar 2,78% 1027,8 27,8 27,8 1 2 27,18 26,41 946,64 27,8/(1 + 0,0229) 27,8/(1 + 0,0259)2 1000,23 1027,8/(1 + 0,0278)3

27,8/(1 + 0,0259) , ,8/(1 + 0,0278)3.")

21

Zero-coupon rente

22

Marktconforme staatsobligatie 09/11 – 2,59%

Yieldcurve: 1 jaar 2,29% 2 jaar 2,59% 3 jaar 2,78 1025,9 25,9 1 2 Koers?

23

Zero-couponrente – bootstrapping

Yieldcurve: 1 jaar 2,29% 2 jaar 2,59% 3 jaar 2,78 1025,9 25,9 1 2 2,29% ?% 25,32 ? 1000,- 974,68 x (1 + ‘2-jrs zero couponrente’)2 = 1025,9 2 jrs zero couponrente: 2,5939%

2 = 1025,9. 2 jrs zero couponrente: 2,5939%")

24

Zero-couponrente – bootstrapping Marktconforme staatsobligatie 08/11 – 2,78%

Yieldcurve: 1 jaar 2,29% 2 jaar 2,59% 3 jaar 2,78% 1027,8 27,8 27,8 1 2 2,29% 2,5939% ?% 27,18 26,41 ? 1000,- 946,41 x (1 + ‘3-jrs zero couponrente’)3 = 1027,8 3 -jrs zero couponrente: 2,7881%

3 = 1027,8. 3 -jrs zero couponrente: 2,7881%")

25

Zero-couponrente – conceptuele uitleg

Yieldcurve: 1 jaar 6% 2 jaar 7% 1070 ? 70 1 2 1 2 7% 7% ?% 65,42 934,58 1000,- 1000,-

26

Vergelijken Eindwaarde van de beleggingen moeten gelijk zijn

Eindwaarde coupondragende obligatie EUR 1070 EUR 70 + herbeleggingrente tweede jaar (?)

")

27

Zero-couponrente Herbeleggingsrente = forwardrente (circa 8%)

Eindwaarde obligatie is dus: EUR % x EUR 70 = EUR 75,6 EUR 1145,60 Rendement zero-couponobligatie 1145,60 / (1 + zero-couponrente)2 = 1000 zero-couponrente = 7,035348

2 = zero-couponrente = 7,")

28

Vorm van de yieldcurve Normale yieldcurve: zero-couponcurve is steiler (zero-rentes zijn hoger) Inverse yieldurve: zero-couponcurve is meer invers (zero-rentes zijn lager) Vlakke yieldcurve: zero-couponcurve ook vlak (zero-rentes gelijk aan gewone rente)

Vlakke yieldcurve: zero-couponcurve ook vlak (zero-rentes gelijk aan gewone rente)")

29

Zero-couponrentes en effectief rendement

Zerocouponrentes: bereken van de contante waarde van afzonderlijke cashflows Hieruit volgt een koers (niet nodig bij beursproducten) Mbv de koers en de cashflows kan het effectief rendement (internal rate of return) worden berekend

Mbv de koers en de cashflows kan het effectief rendement (internal rate of return) worden berekend.")

30

Berekenen effectief rendement – 1 berekenen huidige waarde mbv zero-coupon rates

1040 40 40 1 2 38,83 37,63 946,53 1023,00 40/(1 + 0,03) 40/(1 + 0,031)2 1040/(1 + 0,0319)3

40/(1 + 0,031) /(1 + 0,0319)3.")

31

Berekenen effectief rendement -2 irr berekenen mbv huidige waarde en toekomstige cashflows

1040 40 40 1 2 1023,00,- 40/(1 + r) 40/(1 + r)2 1040/(1 + r)3 1023,0 = 40 (1+r) + 40(1+r) (1+r)3 => er = 3,18

40/(1 + r) /(1 + r) ,0 = 40 (1+r) + 40(1+r) (1+r)3 => er = 3,18.")

32

Waarderen floating rate note

33

Marktwaarde FRN 100 + 6m-EURIBOR 2,5

3 4 5 Wat is op dit moment in de toekomst de koers van de rest van de FRN?

34

Marktwaarde FRN 102,5 1 2 3 4 5 Makkelijke manier om FRN te waarderen (Ook handig om duration te bepalen)

.")

35

Clean price en dirty price

36

Staatsobligatie 02/12 – 5% - waarderen per jul 2010

Yieldcurve: 6m: 4% (182d) 1 jaar 4,25% z.c. 2 jaar 4,35% z.c. Dus: 1,5 jaar 4,30% (547d) 50 50 Jan ‘11 Jan ’12 CW = 50 / ( /360*0,04) = 49,01 CW = 1050 / (1,043)547/365 = / 1, = 985,80 Som CW = 49, ,80 = 1034,81 Koers in de krant: 1009,88 ?????

1 jaar 4,25% z.c. 2 jaar 4,35% z.c. Dus: 1,5 jaar 4,30% (547d) Jan ‘11. Jan ’12. CW = 50 / ( /360*0,04) = 49,01. CW = 1050 / (1,043)547/365 = 1050 / 1, = 985,80. Som CW = 49, ,80 = 1034,81. Koers in de krant: 1009,88")

37

Dirty price en clean price

Dirty price = som contante waarde van de cashflows Clean price = Dirty price -/- opgelopen rente Dirty price = 1034,81 Opgelopen rente = 1000 * 182/365 * 0,05= 24,93 Clean price = 1034,81 – 24,93 = 1009,88

38

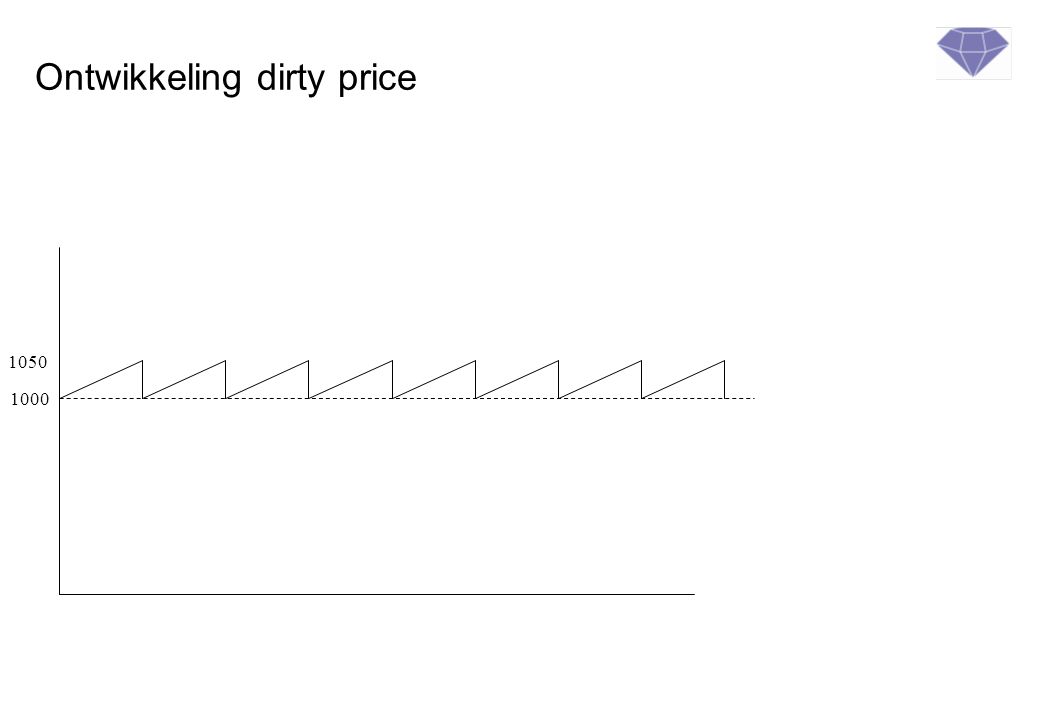

Ontwikkeling dirty price

1050 1000

39

Duration

40

Marktwaarde bond (effectief rendement: 5,9%)

1060 60 60 60 60 1 2 3 4 5 5,9% 5,9% 5,9% 5,9% 5,9% 56,65 53,50 50,52 47,71 795,84 ‘contante waarde’ (1/(1+n)N 1004,22

N. 1004,22.")

41

Marktwaarde bond na rentedaling (effectief rendement 5,8%)

1060 60 60 60 60 1 2 3 4 5 5,8% 5,8% 5,8% 5,8% 5,8% 56,71 53,60 50,66 47,89 799,61 ‘contante waarde’ = 1/(1 + r)n x cashflow 1008,47

n x cashflow. 1008,47.")

42

Duration Rente omlaag -> koers omhoog

Hoeveel? -> factor: duration % verandering koers = duration x renteverandering ,421% = duration x ,1% ,21 Hoe bepaal je de duration?

43

Deus ex machina: formule (modified) duration

contante waarden cashflows x looptijd Duration = 1 / (1+r) x contante waarden = 1/1,059 x 4,46 = 4,21 Correctiefactor

x. contante waarden. = 1/1,059 x 4,46 = 4,21. Correctiefactor.")

44

Afleiding van de modified duration formule

Koers = C1 / (1 + r*)1 + C2 / ( 1 + r*)2 + …… Cn / ( 1 + r*)n Duration proc. koersverandering / renteverandering in % ofwel duration = Δk/k / Δr bij zeer kleine veranderingen: dk/k / dr ofwel duration = dk/dr / k dk/dr = -1C1 / (1 + r)2 -2 x C2 / ( 1 + r) n x Cn / ( 1 + r)n+1 dk/dr / k = contante waarden cashflows x looptijd 1 / (1+r*) x contante waarden * Effectief rendement

1 + C2 / ( 1 + r*)2 + …… Cn / ( 1 + r*)n. Duration proc. koersverandering / renteverandering in % ofwel duration = Δk/k / Δr bij zeer kleine veranderingen: dk/k / dr ofwel duration = dk/dr / k. dk/dr = -1C1 / (1 + r)2 -2 x C2 / ( 1 + r) n x Cn / ( 1 + r)n+1. dk/dr / k = contante waarden cashflows x looptijd. 1 / (1+r*) x. contante waarden. * Effectief rendement.")

45

Verband effectief rendement en koers van obligatie: positieve convextiy

Richtingscoëfficient = duration 1008,47 5,8 Effectief rendement 5,9

46

Basispoint value / delta / PV01

Waardeverandering bij rentestijging met 1 basispunt Portefeuille obligaties van EUR 100 mln, duration 7 jaar Als rente stijgt met 0,01%, daalt de waarde met: 0,01% x EUR x 7 = EUR Voordeel van werken met BPV: risico’s optellen en aftrekken Klant heeft ook een portefeuille medium term notes van EUR 50 mln en een duration van 3 Klant heeft een portefeuille verkochte bundfutures van EUR 100 mln met een duration van 8,5 (positieve BPV)

")

47

Waardering van IRS

48

Waarderen receiver´s renteswap, vaste coupons

Principal EUR 100 mln Oorspronkelijke looptijd 2 jaar Resterend looptijd 1 jr 3 mnd Fixe poot 4% Variabele poot 6mnds EURIBOR 4 4 3m 9m 1y3m afsluiten waarderen Opgelopen rente Clean market value Gross market Value

49

Waarderen receiver´s renteswap, variabele coupons

Principal EUR 100 mln Oorspronkelijke looptijd 2 jaar Resterend looptijd 1 jr 3 mnd Fixe poot 4% Variabele poot 6mnds EURIBOR, 2e fixing 3% (183 dagen) Laatste fixing variabel 4 4 3m 9m 1y3m 1,541 ? ? Nog onbekende cashflows afsluiten Variabele coupon: 100m x 3% x 183/360 = waarderen

Laatste fixing variabel m. 9m. 1y3m. 1,541. Nog onbekende cashflows. afsluiten. Variabele coupon: 100m x 3% x 183/360 = waarderen.")

50

Waarderen receiver´s renteswap, EUR 100 mln

Huidige rentes: 3-maands EURIBOR 2,5% (a/360, 92d) 9-maands EURIBOR 2,80% (a/360, 273d)) 3 tegen 9 forward 2,9337 1 jr 3 mnd 3% zc (30/360,450d = 2,96% a/360,457d) 9 tegen 15 forward 3,1432 4 4 3m 9m 1y3m 1,525 1,475 1,606 afsluiten Berekening nog onbekende cashflows 100m x 181/360 x 2,934 = EUR 100m x 183/360 x 3,169 = EUR waarderen

9-maands EURIBOR 2,80% (a/360, 273d)) 3 tegen 9 forward 2, jr 3 mnd 3% zc (30/360,450d = 2,96% a/360,457d) 9 tegen 15 forward 3, m. 9m. 1y3m. 1,525. 1,475. 1,606. afsluiten. Berekening nog onbekende cashflows. 100m x 181/360 x 2,934 = EUR m x 183/360 x 3,169 = EUR waarderen.")

51

Waarderen vaste coupons

Huidige rentes: 3-maands EURIBOR 2,5% (a/360, 92d) 9-maands EURIBOR 2,80% (a/360, 273d)) 1 jr 3 mnd 3% zc (30/360,450d) 4 4 2 1 CW = / ( /360 x 0,025) = waarderen CW = / ((1,03) 450/360 = / 1,03764 = Totaal:

9-maands EURIBOR 2,80% (a/360, 273d)) 1 jr 3 mnd 3% zc (30/360,450d) CW = / ( /360 x 0,025) = waarderen. CW = / ((1,03) 450/360 = / 1,03764 = Totaal:")

52

Waarderen variabele coupons

Huidige rentes: 3-maands EURIBOR 2,5% (a/360, 92d) 9-maands EURIBOR 2,80% (a/360, 273d)) 1 jr 3 mnd 3 zc% (30/360,450d) 4 4 3m 9m 1y3m 1,525 1,475 1,611 afsluiten 1.541,944 / (1 + 92/360 x 0,025) = ,23 / ( /360 x 2,80) = 1.444,352 / (1,03) 1, = ,38 Totaal: ,34

9-maands EURIBOR 2,80% (a/360, 273d)) 1 jr 3 mnd 3 zc% (30/360,450d) m. 9m. 1y3m. 1,525. 1,475. 1,611. afsluiten ,944 / (1 + 92/360 x 0,025) = , / ( /360 x 2,80) = 1.444, / (1,03) 1,25 = ,38. Totaal: ,34.")

53

Waarderen receiver´s renteswap, opgelopen vaste rente

Principal EUR 100 mln Oorspronkelijke looptijd 2 jaar Resterend looptijd 1 jr 3 mnd Fixe poot 4% Variabele poot 6mnds EURIBOR, 2e fixing 3% 4 4 1y3m 3m Afsluiten = Laatste fixing vast waarderen Opgelopen vaste rente over 9 maanden: 4% x 270/360 x 100m = 3mln :

54

Waarderen receiver´s renteswap, opgelopen variabele rente

Oorspronkelijke looptijd 2 jaar Resterend looptijd 1 jr 3 mnd Fixe poot 4% Variabele poot 6mnds EURIBOR, 2e fixing 3% 4 4 1y3m 3m 1,525 Laatste fixing variabel waarderen Opgelopen variabele rente in huidige coupon 3% x 91/360 x 100m =

55

Waarderen receiver´s renteswap, vaste coupons

PV = 4,000,000 / (1 + 92/360 x 0.025) = 3,974,606.68 Total: ,829,509.73 4 mio 4 mio 3m 9m 1y3m 1,541,944 1,606,513 1,475,021 contract date valuation date PV = 1,541,944 / (1 + 92/360 x 0.025) = 1,532,155.23 PV = 1,475,021 / ( /360 x 0.028) = 1,444,352.29 PV = 1,606,513 / = 1,548,238.38 Total: 4,524,746.34

= 3,974, Total: 7,829, mio. 4 mio. 3m. 9m. 1y3m. 1,541,944. 1,606,513. 1,475,021. contract date. valuation date. PV = 1,541,944 / (1 + 92/360 x 0.025) = 1,532, PV = 1,475,021 / ( /360 x 0.028) = 1,444, PV = 1,606,513 / = 1,548, Total: 4,524,")

56

Totaal te verrekenen Contante waarde vaste coupons: 7.829.509

Contante waarde variabele coupons: ,746.34 Te verrekenen bij unwind ,40 (kredietexposure) Waarvan opgelopen rente (reeds in de boeken) (Clean) Marktwaarde ,39

Waarvan opgelopen rente (reeds in de boeken) (Clean) Marktwaarde ,39.")

57

Duration receiver’s renteswap - looptijd 1,25 jr, 4% tegen 6mnds EURIBOR

1y3m Gewogen cashflows vallen tegen elkaar weg: dus duration is ca. 0 ????

58

Duration van IRS bepalen

Hoe verandert de waarde van de cashflows bij een renteverandering? Probleem bij renteswaps: bij een renteverandering veranderen ook de geprognosticeerde cashflows zelf! Oplossing: bekijk IRS als combinatie van twee tegengestelde leningen

59

Duration receiver’s renteswap - looptijd 1,25 jr, 4% tegen 6mnds EURIBOR

104 4 3m 9m 1y3m 1,525 6m-EURIBOR m-EURIBOR

60

Duration receiver’s renteswap - looptijd 1,25 jr, 4% tegen 6mnds EURIBOR

104 Duration ca 1,15 4 3m 1y3m Duration 0,25 101,525

61

waarde irs-yield Positieve convexity bij receivers’ swaps

Richtingscoëfficient = duration irs-yield 3,9 4

62

waarde irs-yield Negatieve convexity bij payers’ swaps

Richtingscoëfficient = duration 3.9 irs-yield 4

63

Agenda trainingsdagen 2011 – eerste halfjaar

Rentederivaten 3 en 10 februari Waardering en Rapportage 6 en 13 april Valutaderivaten 5 en 12 april Fundamentals of FX en Money Markets 8 en 16 februari ACI Dealing Certificate 13, 20 jan, 3, 10 feb ACI Diploma 10, 17, 24 en 31 jan CFA level 1 16 dec 2010, 6 en 27 jan, 17 feb, 10 en 31 mrt, 21 april, 19 en 20 mei

Verwante presentaties

Quiz Night !>")